Home » Posts tagged 'Huawei'

Tag Archives: Huawei

Huawei’s All Cloud Networks with a Cloud-based Wireless Network (CloudAir) supporting new radio access technologies in a new architecture (CloudRAN), and network slicing in particular, for upcoming 5G, Future Internet, and In-Network Computing

April 6, 2017, Huawei Carrier Business YouTube channel: All Cloud Network Towards 5G (2½ min)

IT, cloud computing, and the Internet are reshaping the world. Video, cloud services and IoT are also revolutionizing our lifestyle. How can carriers quickly launch new services? How can they achieve business agility? How will they optimize cost structure? These are the three biggest concerns of carriers on the transformation path to All Cloud Networks.

During the process of full cloudification, carriers will have to cloudify equipment, networks, services and the whole operational system if they want to deliver real ROADS experience. Huawei launched its All Cloud strategy in order to help operators succeed in transformation.

All Cloud Network use the principles and technologies of the cloud to reconstructs carrier networks with pooled hardware resources, fully distributed software architecture, and full automation operations for more efficient utilization, more agile services and higher operational efficiency.

April 6, 2017, Huawei Carrier Business YouTube channel: ROADS to New Growth (1½ min) (more…)

Smartphone market outlook and the MediaTek Helio X10 based Xiaomi Redmi Note 2/Prime launched for $125, $140 and $156

Let’s start with an extremely good presentation video by Mrwhosetheboss:

And an actual experience video from Chinese sources (finished by comparing to iPhone 6):

Aug 16, 2015, Xiaomi Today: Xiaomi sold 800,000 Redmi Note 2 phones in 12 hours

Note that Xiaomi has already been the top Chinese company tracked here:

– Dec 12, 2012: UPDATE Aug’13: Xiaomi $130 Hongmi superphone END MediaTek MT6589 quad-core Cortex-A7 SoC with HSPA+ and TD-SCDMA is available for Android smartphones and tablets of Q1 delivery

– Aug 1, 2013: Xiaomi, OPPO and Meizu–top Chinese brands of smartphone innovation

– Aug 30, 2013: Assesment of the Xiaomi phenomenon before the global storm is starting on Sept 5

– Sept 5, 2013: Xiaomi announcements: from Mi3 to Xiaomi TV

– June 12, 2014: Xiaomi’s global offensive with Hugo Barra in charge is threatening Apple—with 10.4 million smartphones sold in China it had already outsold Apple in Q1’14, having “just” 9 million iPhones sold there from which we must at least understand the market situation in China upto Q1 2014 as the reference for the Xiaomi’s progress presented here:

With the Q3 2015 Redmi Note 2/Prime advancement Xiaomi will kill the much hoped (by some stock market analysts) incremental opportunities for the $199 Apple iPhone 6 and $299 iPhone 6 Plus in China and throughout the world. And recall that those were announced 11 months ago as “The Biggest Advancements in iPhone History“

This report is similar to later Canalys findings: Xiaomi 15.9%, Huawei 15.7%, and Apple #3. But for the rest: #4 Samsung, #5 vivo. Globally Xiaomi became the #2 Chinese smartphone brand in Q2 2015 according to TrendForce with 5.9% market share, the #1 Huawei having 7.6%, but first time surpassing Lenovo, as well as continuing to distance itself from TCL (Alcatel) and OPPO. Similar to data from Counterpoint Research. See Chinese OEMs Rule. Considering Huawei’s aggressive push since 2011, when Xiaomi devices started in China, Xiaomi’s global achievement is a very remarkable feat.

Why? Because being in the smartphone device business for just 4 years Xiaomi has already been on or around the top in China for the last 12 months, as well as has launched an impressive global march.

That global sales campaign has been going on in Asia, Russia and Turkey so far, but it is now expanding to Latin America with new model launching in Brazil [CCTV America YouTube channel, July 14, 2015]: “The world’s third largest smartphone maker is taking a different approach in its plans for global domination. Instead of looking to expand in the obvious markets like the U.S. and Europe, Xiaomi is looking to South America. CCTV’s Paulo Cabral filed this report from Sao Paulo.”

And it is not difficult to foresee a huge global success for the company as in India Xiaomi became “the 5th biggest seller of phones in the country, a feat accomplished in only 8 months“: Smartphone company Xiaomi expanding to India and beyond [CCTV America YouTube channel, March 20, 2015]

And now China’s Xiaomi Begins Making Smartphones in India [Voice of America, Aug 14, 2015]: “Xiaomi’s Redmi2 Prime smartphone [NOT the Note 2 one], priced at about $110, began rolling out from a factory in Sri City in southern Andhra Pradesh state this week. … entered the Indian market just a year ago, but since then price conscious consumers have snapped up 3 million phones.“

Also this all happened after “The Chinese smartphone maker, Xiaomi, held a second flash sale of its new 4.7″ Redmi 1S [at $110/699 RMB almost of the same price level as this year’s $125/799 RMB Redmi Note 2] on Tuesday [Sept 9, 2014], after selling out in just four seconds a week ago.“: Chinese smartphone Xiaomi competes with Apple [CCTV America YouTube channel, Sept 9, 2014]

from which I will include the following Q2 CY2014 market share slide for China here:

as this position of being “on the top or around it” has been kept by Xiaomi ever since.

Then we should not forget what only 8 months ago was introduced as Xiaomi launches MiNote, a new iPhone competitor [CCTV America YouTube channel, Jan 15, 2015]: “The tech world is abuzz about Chinese tech company Xiaomi’s bid to compete with Apple and Samsung. Xiaomi CEO Lei Jun unveiled the MiNote and MiNote Pro [at $313/1999 RMB and $391/2499 RMB a kind of twice as expensive predecessors to the new Redmi Note 2/Prime] on Thursday, both are cheaper than similar iPhone models. CCTV’s Xia Cheng reported this story from Beijing.”

Finally we should look at the new specification comparisons by GSMinsider:

With that Xiaomi will kill Samsung high-end opportunities as well.

Let’s look first at the quite drastic decline of the Samsung smartphone business for the last year and a half (data from Strategy Analytics as it’s been represented in the Apple and Huawei move on Samsung article of July 30, 2015 from Telecom.com, with the vendor rankings in the table according to the latest quarter, i.e. Q2 2015):

Note that Coolpad (Yulong) and ZTE are also globally represented Chinese brands, not mentioned so far in this article.

Which unit-wise looks like as follows (in millions):

Then I can again refer to Samsung-related high-end specification comparisons produced by GSMinsider:

And don’t be fooled with the Qualcomm Snadragon 805 and 801 SoCs used by Samsung in these 2014 vintage devices as Samsung itself abandoned Qualcomm as an SoC supplier for its 2015 devices:

Note: Such Samsung move of abandoning the Qualcomm Snadragon 805 and 801 SoCs in its latest high-end products is not an accident but a hard-pressed necessity. The octa-core Qualcomm Snadragon 810 replacing the 805/801 had serious thermal throttling problems, and the Chinese brands were starting to use other octa-cores, among them the quite competitive MediaTek Helio X10. See the following Q1 2015 technology landscape presentation composed of the graphical views from the April 12 and April 24 reports by CINNO Research (in addition to the camera related view on the right):

Note: Such Samsung move of abandoning the Qualcomm Snadragon 805 and 801 SoCs in its latest high-end products is not an accident but a hard-pressed necessity. The octa-core Qualcomm Snadragon 810 replacing the 805/801 had serious thermal throttling problems, and the Chinese brands were starting to use other octa-cores, among them the quite competitive MediaTek Helio X10. See the following Q1 2015 technology landscape presentation composed of the graphical views from the April 12 and April 24 reports by CINNO Research (in addition to the camera related view on the right):

And software-wise Xaomi is already 5 years in the smartphone business with a lot of quite enthusiastic supporters for its Android based Mi User Interface throughout the world. The MIUI 5th Anniversary: Greetings From MIUI Fans From All Over The World testimonial video from the MIUI ROM YouTube channel dated August 12, 2015 is stating that: “MIUI is one of the most popular Android ROMs in the world. It is based on Android, featuring a rich user experience and user customizable themes. MIUI is updated every Friday based on feedback from its users. Now with over 100 million users and 34 MIUI fan sites worldwide, MIUI is the choice of many Android users globally.“

What kind of “much hoped incremental opportunities (by some stock market analysts) for Apple” I was talking about?

From India Will Overtake US to Become World’s Second Largest Smartphone Market by 2017 [July 1, 2015] by Strategy Analytics the following chart has been produced for Dazeinfo’s Global Smartphone Sales 2015 – 2017: India Will Surpass The US [July 1, 2015] report:  That chart has been used by Brian Nichols in his Why Apple’s Growth-Related Fears Are Overblown [Aug 12, 2015] article on Seeking Alpha for its final argument that:

That chart has been used by Brian Nichols in his Why Apple’s Growth-Related Fears Are Overblown [Aug 12, 2015] article on Seeking Alpha for its final argument that:

… the market sees China as imperative to Apple’s future growth outlook and while true at the moment, there’s a catalyst forming that should lessen the company’s reliance on China and lead to many millions of new iPhone sales.

…

China is not that “forming catalyst” that I mentioned earlier. Instead, Apple has a prime opportunity to grow in India over the next year or two, a market that’s growing rapidly with middle class consumers and is the world’s second largest economy by population behind only China.…

… with India’s help, which includes the growth in middle class consumers through 2020, India might very well one day become just as important as China to Apple.

Before coming to such final argument Nichols is talking about the current market situation in China via a chart from Above Avalon’s China Mobile Is a Game Changer for Apple [April 29, 2015] research note and with the following comments around that:

I expect Apple to find additional growth in China next year, regardless of what has transpired from a macro perspective over the last few months. The reason is simple: Improved network coverage. Fact of the matter is that most Chinese consumers are still using 2G or 3G networks, which are hardly compatible with the iPhone 6. At the end of the first quarter, China Mobile (NYSE:CHL) had 153 million 4G customers, up from 90 million in December of 2014 and just 1.3 million in February of 2014. However, China Mobile had 815 million total customers. So that means the majority of its subscribers are still on 2G or 3G networks. Given the rate at which China Mobile has added 4G customers during the last 16 months, investors can rest assured that its network and 4G customers will be far larger by this time next year. Notably, most of those 4G customers will need smartphones, and Apple has quickly become the most popular choice in China.

As for China’s second and third largest wireless carriers, China Unicom (NYSE:CHU) and China Telecom (NYSE:CHA), they have nearly 500 million customers collectively. And believe it or not, China Unicom and China Telecom’s 4G network is even more underdeveloped than China Mobile’s network. However, both China Unicom and China Telecom are working just as fast to build their respective 4G networks. Once more, this increases Apple’s market opportunity in China, and is the key reason why I think Apple’s growth in China will continue through next year, probably at a very high double-digit rate.

So these are the speculations which IMHO do not take into account the new product waves from major Apple and Samsung competitors, especially Xiaomi.

Xiaomi’s new 5.5″ Redmi Note 2 launched in China just this week for $125/799 RMB (16GB version supporting TDD-LTE for a China specific 4G version of LTE as well as TD-SCDMA, the China specific 3.5G — targeted at China Mobile subscribers) and $140/899 RMB (16GB version supporting both TDD-LTE and FDD-LTE, i.e. both 4G versions — for the subscribers of any mobile operators, and especially of China Unicom and China Telecom) is the actual case in this regard. Watch the Xiaomi Redmi Note 2 Prime first look miui 7 pre-order video direct from the launch (the QR code at the start and the end has been positioned out of my embedded view):

Announced: August 13 2015

|

Sound Alert Types:

|

The 2.2 GHz Redmi Note 2 Prime version with 32GB storage and support of TDD-LTE + FDD-LTE will sell at $156 (999 RMB).

More information:

– Aug 13, 2015: All About Redmi Note 2/Prime: Specifications, Price, Hands-on Pictures! review by Xiaomi MIUI Official Forum

– Aug 13, 2015: Xiaomi New Product Launch: MIUI 7(China), Redmi Note 2(Prime), Mi Wi-Fi nano full launch information (not only the Redmi Note 2/Prime) by Xiaomi MIUI Official Forum, from which the major Redmi Note 2 and 2 Pro Android competition (Huawei P8 and P8max with Hisilicon Kirin 930 and 935 SoCs, and Meizu MX5 (with the same MediaTek Helio X10 @2.2 GHz) on the Chinese market is described as:

Note: regarding the benchmarked performance of each SoC I will recommend the results made available in the Exynos 7420 vs Snapdragon 810 vs MediaTek Helio X10 Turbo MT6795T vs Hisilicon Kirin 935: Benchmark Scores [July 3, 2015] GSMinsider article

– For a much broader competitive comparison I will recommend the Redmi Note 2’s comparisons by GSMinsider which currently contains comparisons (spec-wise):

Aug 13, 2015: Additional videos from XiaomiHK YouTube channel:

Xiaomi – MIUI Introduction (with English subtitles)

Xiaomi – MIUI V7 Endurance

i.e. MIU 7 on [Xiaomi’s] Mi 4, Huawei Honor 6, Meizu MX4 and Samsung Galaxy S5

Xiaomi – MIUI V7 Performance

Xiaomi – RedmiNote2″>Xiaomi – RedmiNote2

Xiaomi – RedmiNote2 Camera

Important videos available on the Bloomberg Business website only, with 3 most important videos added to them from the CCTV America YouTube channel:

June 5, 2014: Here’s Why Hugo Barra Left Google to Be Xiaomi VP: Xiaomi Early Investor Robin Chan discusses Xiaomi’s hiring of Google’s Hugo Barra on Bloomberg Television’s “Bloomberg West.” Former Xiaomi Board Member Hans Tung also speaks.

July 17, 2015: Xiaomi’s Hugo Barra: Studio 1.0 (Full Show 7/16): This week on Studio 1.0: Emily Chang sits down with Hugo Barra, vice president of global operations at Xiaomi. (Source: Bloomberg) 21 minutes from which I will include here the only slide displayed

Plus a lot of other unique information is available in that interview: like the 2015 vintage business model of Xiaomi (investments into non-platform startups to build business partnerships, a whole ecosystem around Xiaomi etc.).

I will add to that the product shown in the Bloomberg interview as an example of such ecosystem generation. This has been documented in Xiaomi launches $13 fitness band [CCTV America YouTube channel, Aug 18, 2014] as: “Chinese Smartphone maker Xiao-mi has started selling an interactive wristband called the Mi Band. The device can measure one’s heart rate and monitor sleep patterns. It’s not the first such device to hit the market, but so far, it’s the cheapest.”

I will also add the Xiaomi Buying Spree Gives Apple, Samsung Reason to Worry [Bloomberg Business YouTube channel, Jan 8, 2015] video stating that: “Xiaomi zoomed past Apple Inc. and Samsung in China smartphone sales just three years after releasing its first model. Founder Lei Jun is now on a buying spree to take that momentum beyond handsets. Bloomberg’s Edmond Lococo has more on “On The Move Asia.” (Source: Bloomberg)”

Then remember the already known facts mentioned in the second video on the Bloomberg website like: “Xiaomi is not Apple“, “Xiami is an Internet company” (“an Internet platform and services brand” heard in another interview), “services are inherent part of Xiaomi“, “Xiaomi is one of the biggest e-commerce sites in China“, “the Xiaomi platform products are enhanced in functionality on requests from its users by around 50%” etc.

As the latest proof-point of such an Internet platform and service strategy of the company watch the Chinese mobile co. Xiaomi launches wallet app [CCTV America YouTube channel, March 26, 2015] video:

Other videos from Bloomberg Business YouTube channel:

Jan 15, 2015: Xiaomi’s Rapid Rise to $45B Valuation Topping Uber: Xiaomi is Apple and Samsung’s rapidly growing threat. Now the world’s third-largest smartphone maker, Xiaomi is releasing its next phone on Thursday at an event in Beijing. Bloomberg’s Cory Johnson looks at how just fast this company is growing. (Source: Bloomberg)

June 5, 2014: Meet the Billionaire ‘Steve Jobs of China’ Lei Jun: Xiaomi co-founder and chief executive officer Lei Jun is known as the Steve Jobs of China, complete with a wardrobe of black shirts and a cult following. But what did he do before starting Xiaomi, and how has his personality helped drive Xiaomi’s success? Bloomberg West’s Emily Chang gives us an overview of this rock star CEO.

Jan 5, 2015: Xiaomi Doubles Revenue to $12B as Phone Sales Triple: Xiaomi, whose investors include billionaire Yuri Milner, more than doubled its revenue in 2014, according to a blog posting by CEO Lei Jun.

Feb 13, 2015: Xiaomi’s Barra: U.S. Market Is Important in Many Ways: Xiaomi’s Hugo Barra discusses the company’s global expansion plans with Bloomberg’s Brad Stone on “Bloomberg West.”

June 4, 2015: Xiaomi Grows Wearable Device Market Share: Xiaomi is looking to elbow its way into the wearable device market. New figures suggest it took a quarter slice of global sales the first three months of the year. Bloomberg Intelligence’s Jitendra Waral discusses the sales figures on “Trending Business.”

Other videos from the CCTV America YouTube channel:

July 22, 2014: Hugo Barra on latest Xiaomi products: Chinese tech firm Xiaomi showed off some of its latest products on Tuesday. The Beijing-based company unveiled its new Mi smartphone and billed it as a challenger to Apple’s iPhone. Analysts say the Mi 4 will be a make or break product for Xiaomi after sales of the older model proved disappointing.The company is also aggressively expanding overseas. Hugo Barra, Xiaomi’s Vice President for overseas business spoke with CCTV’s Xia Cheng.

July 14, 2015: Eric Schiffer on Xiaomi’s global strategy: For more on Xiaomi’s global strategy, CCTV’s Michelle Makori spoke to Eric Schiffer, CEO of Patriarch Equity.

Dec 22, 2014: Tech company Xiaomi flourishes in China, India despite patent disputes: China’s Xiaomi tech company is often compared to Apple. Founded in 2010, Xiaomi has quickly surpassed Samsung to become the top smartphone in China and third in the world. Xiaomi phones are currently only sold online and in China and India.

Dec 22, 2014: Ari Zoldan of Quantum Networks discusses Chinese companies, patent troubles: CCTV America’s Sean Callebs interviewed tech industry expert and CEO of Quantum Networks Ari Zoldan about the rise of Xiaomi and it’s legal battles.

Tablet and smartphone market trends

September update: Qualcomm’s smartphone AP revenues declined 17% year-over-year in the second quarter of 2015, Strategy Analytics estimated. Qualcomm maintained its smartphone AP market share leadership with 45% revenue share, followed by Apple with 19% revenue share and MediaTek with 18% revenue share. For the rest 18%: After a difficult 2014, Samsung LSI continued to recover and more than doubled its smartphone AP shipments in the second quarter of 2015 compared to the same period last year. Samsung LSI capitalised on its Galaxy S6 design-win in Q2 2015. In addition the company featured in multiple mid-range smartphones from Samsung Mobile. Full report: Smartphone Apps Processor Market Share Q2 2015: Samsung LSI Maintains Momentum

… The global tablet AP market declined 28% year-over-year to reach US$679 million in the second quarter of 2015, according to Strategy Analytics. Apple, Intel, Qualcomm, MediaTek and Samsung LSI captured the top-five revenue share rankings in the market during the quarter. Apple led the tablet AP market with 27% revenue share, followed by Intel with 18% revenue share. Qualcomm ranked number three, narrowly behind Intel. ![GT400150821[1]](https://lazure2.wordpress.com/wp-content/uploads/2015/08/gt4001508211.jpg?w=960) Full report: Tablet Apps Processor Market Share Q2 2015: Apple and Intel Maintain Top Two Spots

Full report: Tablet Apps Processor Market Share Q2 2015: Apple and Intel Maintain Top Two Spots

…

Digitimes Research saw global tablet shipments fall to 45.76 million units in second-quarter 2015, showing a 10% decrease on quarter and representing more than a 15% decrease on year. Full report: Global tablet market – 2Q 2015 End of September update

Investors.com comments on tablet and smartphone market trends — Q2’2015: 1. Apple, Samsung lose ground in tablet market — LG and Huawei gain

1. Apple, Samsung lose ground in tablet market — LG and Huawei gain

2. Apple, Huawei [and Xiaomi] buck slowing smartphone sales trend

As the commenting articles by Investors.com are based on press releases of 2 market research companies I will give the web reference here for those press releases themselves, as well as 3 other press releases not commented on by Investors.com (if there are trend indications in the press releases themselves I will copy them alongside the web reference):

- July 29, 2015: Worldwide Tablet Market Continues to Decline; Vendor Landscape is Evolving, According to IDC

“Longer life cycles, increased competition from other categories such as larger smartphones, combined with the fact that end users can install the latest operating systems on their older tablets has stifled the initial enthusiasm for these devices in the consumer market,” said Jitesh Ubrani, Senior Research Analyst, Worldwide Mobile Device Trackers. “But with newer form factors like 2-in-1s, and added productivity-enabling features like those highlighted in iOS9, vendors should be able to bring new vitality to a market that has lost its momentum.”

“Longer life cycles, increased competition from other categories such as larger smartphones, combined with the fact that end users can install the latest operating systems on their older tablets has stifled the initial enthusiasm for these devices in the consumer market,” said Jitesh Ubrani, Senior Research Analyst, Worldwide Mobile Device Trackers. “But with newer form factors like 2-in-1s, and added productivity-enabling features like those highlighted in iOS9, vendors should be able to bring new vitality to a market that has lost its momentum.” - July 30, 2015: Huawei Becomes World’s 3rd Largest Mobile Phone Vendor in Q2 2015 [says Strategy Analytics]

- Woody Oh, Director at Strategy Analytics, said, “… Smartphones accounted for 8 in 10 of total mobile phone shipments during the quarter. The 2 percent growth rate of the overall mobile phone market is the industry’s weakest performance for two years, due to slowing demand for handsets in China, Europe and the US.”

- Neil Mawston, Executive Director at Strategy Analytics, added, “… Samsung has stabilized volumes in the high-end, but its lower-tier mobile phones continue to face intense competition from rivals such as Huawei in Asia. … Apple outperformed as consumers in China and elsewhere upgraded to bigger-screen iPhone 6 and 6 Plus models.”

- Ken Hyers, Director at Strategy Analytics, added, “… Huawei is rising fast in all regions of the world, particularly China where its 4G models, such as the Mate7, are proving wildly popular. Huawei has finally overtaken Microsoft to become the world’s third largest mobile phone vendor for the first time ever.”

- Neil Mawston, Executive Director at Strategy Analytics, added, “Microsoft shipped 27.8 million mobile phones and captured 6 percent marketshare worldwide in the second quarter of 2015. Microsoft’s 6 percent global mobile phone marketshare is sitting near an all-time low. Microsoft continues to lose ground in feature phones, while its Lumia smartphone portfolio is in a holding pattern awaiting the launch of new Windows 10 models later this year. Xiaomi shipped 19.8 million mobile phones and captured 5 percent marketshare worldwide in Q2 2015. Xiaomi remains a major player in the China mobile phone market, but its local and international growth is slowing and Xiaomi is facing intense competition from Huawei, Meizu and others. As a result, Xiaomi may struggle to hold on to its top-five global mobile phone ranking in the coming quarters.”

- June 17, 2015: Business smartphones shipments in Q1 up 26% from last year, now 27% of total smartphone market [says Strategy Analytics]

Android was the most dominant OS in terms of business smartphone shipments in Q1, accounting for nearly 60% of all business smartphones (corporate- and personal-liable). It was also the dominant BYOD device; 68% of personal-liable shipments in Q1 were Android. Apple iOS accounted for only 27% of BYOD shipments in Q1, but was the dominant platform in terms of corporate-liable smartphones, with 48% of Q1 CL shipments. The difference in Android/iOS shipments between the CL and IL categories reflects the continuing corporate perception that iPhones are “safer” than Android-based devices.

Android was the most dominant OS in terms of business smartphone shipments in Q1, accounting for nearly 60% of all business smartphones (corporate- and personal-liable). It was also the dominant BYOD device; 68% of personal-liable shipments in Q1 were Android. Apple iOS accounted for only 27% of BYOD shipments in Q1, but was the dominant platform in terms of corporate-liable smartphones, with 48% of Q1 CL shipments. The difference in Android/iOS shipments between the CL and IL categories reflects the continuing corporate perception that iPhones are “safer” than Android-based devices.

- Shipments of personal-liable smartphones (i.e. “bring your own device,” or BYOD, phones) drove market growth in Q1

- Strategy analytics defines personal-liable devices as devices purchased by the end-user and expensed back to the company or organization, or devices purchased outright by individual users but used primarily for business purposes linking to corporate applications and backend systems.

- While personal liable devices dominate worldwide business smartphone shipments, some regions are more resistant to the BYOD trend than others. Such regions include Western Europe and Central Europe, where corporate-liable devices are the dominant types of business smartphones. In Western Europe in Q1, 61% of the 10 million business smart phones were corporate-liable. Central and Eastern Europe had a slightly higher rate of BYOD devices shipped in Q1 — 41% — but the majority of smartphones shipped in this regions was also corporate-liable. This a sharp contrast to North America, where three-quarters of business smartphone shipments are personal-liable. The trend in Western and Eastern Europe reflects the more corporate-centric approach businesses take to mobility in these regions.

- July 29, 2015: Mobile Broadband Tablet Subscriptions to Double to 200 Million by 2021, says Strategy Analytics

- Strategy Analytics forecasts global mobile data subscriptions on tablets will more than double from 2015 to 2021, reaching over 200 million

- Around the globe, over 100 million wireless connections on cellular enabled tablets will be added through 2021. By 2021 tablets will only account for 2 percent of total mobile subscriptions, a 2.7 percent population penetration rate.

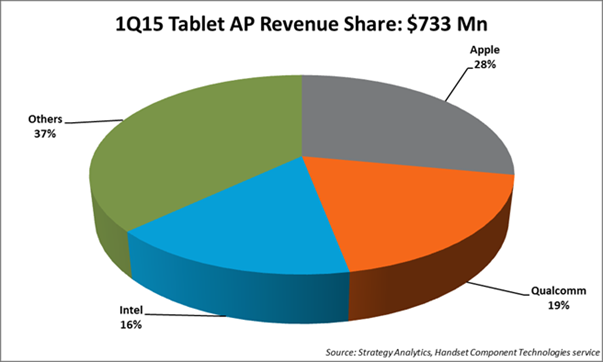

- July 29, 2015: Intel Maintains Top Spot in Non-Apple Tablet Apps Processors in Q1 2015 says Strategy Analytics

⇒The global tablet applications processor (AP) market declined -6 percent year-over-year to reach $733 million in Q1 2015- According to Sravan Kundojjala, Associate Director, “Intel maintained its top spot in the non-Apple tablet AP market in unit terms in Q1 2015. Strategy Analytics estimate Android-based tablets accounted for over 70 percent of Intel’s total tablet AP shipments in Q1 2015. We expect Intel’s Atom X3 cellular tablet chip product line to help Intel maintain its momentum in the tablet AP market.”

- Stuart Robinson, Executive Director of the Strategy Analytics Handset Component Technologies (HCT) service added, “Strategy Analytics estimates that baseband-integrated tablet AP shipments accounted for over one-fourth of total tablet AP shipments in Q1 2015, helped by a strong push from Qualcomm, MediaTek and Spreadtrum. We expect continued momentum for integrated APs as Intel, Rockchip and others join the bandwagon.”

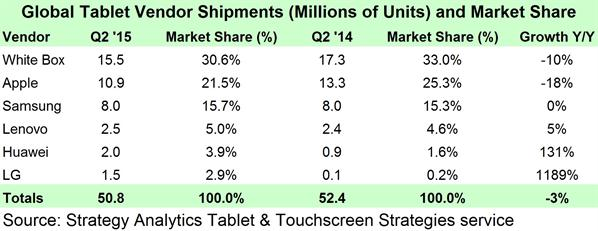

- July 30, 2015: Windows Tablet Shipments Nearly Double in Q2’15, says Strategy Analytics

⇒Global Tablet Shipments and Market Share in Q2 2015 (preliminary)

- Windows-branded Tablets comprised 9 percent of shipments in Q2 2015, up 4 points from Q2 2014

- Android-branded Tablet shipment market share was flat at 70 percent in Q2 2015

- Apple continued its slide in market share down to an all-time low of 21 percent in Q2 2015, 4 points lower than Q2 2014

- Vendors with strong 3G and LTE connected Tablet strategies such as Huawei, LG, and TCL-Alcatel gained market share as leaders like Apple, Samsung, and the White Box community lost ground

Tablet & Touchscreen Strategies Senior Analyst Eric Smith added, “Windows share continues to improve as more models become available from traditional PC vendors, White Label vendors, and Microsoft itself though a healthy Surface lineup and distribution expansion. The key going forward will be if the coming wave of 2-in-1 Detachable Tablets is a hit with consumers or if they go the way of the Netbook—we remain cautiously optimistic on this point.” |

Tablet & Touchscreen Strategies Service Director Peter King said, “Apple’s fortunes will turn around soon as it will launch the 12.9-inch iPad Pro as well as an iPad mini 4 in Q4 2015. New features in iOS 9, which are exclusive to iPad such as multi-tasking and a more convenient soft keyboard, will also help compel upgrades by owners of older iPad models. Meanwhile, Huawei and LG have posted fantastic growth primarily due to well-executed 3G and LTE connected Tablet strategies.” |

Then I will add 2 additional information pieces from Strategy Analytics:

Oct 8, 2014: Replacement Demand to Boost PC Sales in 2015, says Strategy Analytics

Having experienced negative growth since 2012, global PC sales are expected to rise 5 percent in 2015 driven by replacement of an ageing installed base according to Strategy Analytics’ Connected Home Devices (CHD) service report, “Computers in the Post-PC Era: Growth Opportunities and Strategies.”

Click here for the report:

http://www.strategyanalytics.com/default.aspx?mod=reportabstractviewer&a0=10146

- PC sales will fall by 4 percent in 2014 before returning to modest growth in 2015 and beyond to support replacement demand.

- Strategy Analytics’ consumer research of computing device usage in developed markets indicates that PCs remain essential computing devices despite healthy Tablet sales.

- Frequent Tablet usage has grown by 22 percentage points from 2011 to Q4 2013 up to 32 percent of all households while frequent Mobile PC (excluding Tablets) usage has stayed steady through this period, as 63 percent of all households indicated they frequently used Mobile PCs.

- Frequent usage of all PCs (including Mobile and Desktop PCs and excluding Tablets) remained above the 90 percent mark of all households, falling only 3 percentage points during this period.

Quotes:

Eric Smith, Analyst of Connected Home Devices, said: “Multiple PC ownership is falling as Tablet sales supplant replacement demand for secondary PCs mainly used for casual tasks. Still, PCs will remain essential devices as households eventually replace their primary PCs used for productivity tasks such as spreadsheet and video editing or personal banking.”

David Watkins, Service Director, Connected Home Devices, added: “The modern Tablet user experience is quickly arriving on the PC thanks to more affordable 2-in-1 Convertible PCs and new operating systems which blend traditional PC and Tablet user experiences. We see development of these forces aligning perfectly with an older PC installed base ripe for replacement in 2015.”

May 1, 2015: Children Change Disney’s Digital Strategy: “App TV” Now Central To Content Planning by David Mercer

Multiscreen TV behaviour is at the centre of television’s stormy transformation – viewing of broadcast, linear TV on the TV screen is apparently in decline while consumption on smartphones and tablets is increasing. Making sense of the big picture is increasingly challenging, and legacy players like broadcasters and the major content owners are inevitably somewhat resistant to the idea that their traditional businesses are under serious threat.

We have monitored the early stages of this transformation for the past decade and see its results in our own research, and we continue to predict further industry disruption in our forecasts. But sometimes it is only when you hear the evidence given in person by a senior executive at a leading global player that the scale of the challenge and opportunity are finally brought home.

This happened at last week’s AppsWorld event in Berlin, where I chaired the TV and Multiscreen conference. The speaker was Andreas Peters, Head of Digital for the Walt Disney Company Germany, Austria and Switzerland. Andreas presented some of the most compelling evidence I have yet heard that television is truly a multiscreen medium for the next generation of viewers.

Disney’s challenge in Germany was to launch a television show called Violetta aimed at 8-12 year old girls. It had been introduced successfully in Argentina but had failed in the UK. As it often does, Disney had invested considerable amounts in merchandising and retailers were eagerly anticipating sales of the new product lines. The show was first broadcast on German free TV on May 1st 2014 but it achieved only very low ratings.

The question for Disney managers was whether traditional TV had stopped working. A crisis meeting was held with a view to writing off the investment. Disney had previously not made its shows available online in Germany but the Violetta situation was so serious they were persuaded to experiment. Two episodes were made available on Youtube with a link to Disney’s own website. Viewing of the content on Youtube very quickly went viral until Disney had achieved a reach of 50% of 8-12 year old girls and eight million views. Violetta went on to become a success in German-speaking markets.

The evidence was clear: for some shows at least, younger children cannot now be reached using the traditional broadcast TV/big screen model. Peters explained that the Violetta experience was transformative for the Disney organisation and led to the inclusion of online and digital media as a key element in the business case for many products. In fact it also led to the development and launch of Disney’s own Watch App, which includes live streaming and seven-day catch-up programmes from the broadcast Disney Channel.

Even after the Violetta experience Disney was sceptical that an app was needed – there was a feeling that the website would be sufficient. Nevertheless the app was launched and Disney had planned for 20,000 downloads. Instead it has passed one million downloads in its first six months. Peters noted: “This was a real shock for us. We completely underestimated the demand.” Around 500,000 viewers are now using the Disney Watch app for linear television viewing, in addition to millions of shows being downloaded for catch-up viewing. Peak app viewing hours are between 6am and 8am and then between 1pm and 9pm on school days, with a different pattern at weekends. Peters made it clear that children did not want lots of features built in to the app – just like TV, they just want to hit “play” and watch.

“Our TV colleagues of course don’t want to believe this,” said Peters. “But the world has changed and it will continue to change.” Disney has also seen a knock-on effect from its app launch with an increase in free-to-air broadcast TV viewing. But the firm is now clear that mobile is not just an add-on to TV or a promotional tool; it must be an integral part of the entire process.

There are many implications for content strategy. TV and Digital have to “understand each other”, which is a challenge when the KPIs in each world are very different. As we have often heard, the video industry is crying out for a set of common metrics which can apply and support advertisers in both TV and online worlds. Video consumption patterns vary and different content may be relevant to different platforms.

But the overall lesson is clear: “TV” is not just the big screen in the corner of the living room. It must embrace multiscreen distribution strategies in order to reach its maximum potential. TV companies are betraying their audiences and their investors if they don’t target the 6.4bn addressable screens available to them.

The lost U.S. grip on the mobile computing market, including not only the device business, but software development and patterns of use in general

This is my conclusion after the two sections of analysis presented below:

I. China-based white-box tablet and smartphone vendors were shaping the 2013 global device market which will even more so in 2014

II. Asia is following different patterns of mobile use than the United States – the case of China and South Korea

The single, most forceful evidence for all of the above is the extraordinary presentation of Hugo Barra, Vice President, Xiaomi Global & Loic Le Meur, LeWeb Founders- LeWeb’13 Paris – [LeWebYouTube channel, Dec 11, 2013]

I. China-based white-box tablet vendors and smartphone vendors were shaping the 2013 global device market which will even more so in 2014

My analysis of the smartphone market in general was first presented in the Device businesses should have a China-based independent headquarter at least for Asia/Pacific if they want to succeed [‘Experiencing the Cloud’, Jan 28, 2014] and then it was already updated by the recent Chinese smartphone brands to conquer the global market? [‘Experiencing the Cloud’, March 18, 2014] post of mine.

As a Q4’13 update to The tablet market in Q1-Q3’13: It was mainly shaped by white-box vendors while Samsung was quite successfully attacking both Apple and the white-box vendors with triple digit growth both worldwide and in Mainland China [‘Experiencing the Cloud’, Nov 14, 2013] post of mine I should first add here the following analysis:

Note that the white-box tablet shipments from China were estimated by company data and Credit Suisse estimates as 7% and 10% higher: 2012: 58M (vs. 54.4M here), 2013: 98M (vs. 89.1M here) (as per the “Figure 30” chart in this blog below). As you see here and later on the conclusion of the Q1-Q3’13 analysis for the tablet market, represented by the title of the previous post will hold for the whole CY2013 as well. The only remarkable change is the sudden jump in Apple iPad sales in Q4, both worldwide and in China. This is, however, only attributed to Q4 introduction of the new iPad Air which was much anticipated for months, thus postponement of new purchases and the peak when it was available. So, for the whole year, my conclusion still holds true,

Note that the 2013 tablet market in China was 17.2M as per the above data, while the 2013 worldwide tablet market was 219.5M per IDC, and 255M according to company data and Credit Suisse estimates (as per the “Figure 30” chart in this blog below). So China was just 7.8% or 6.4% of the worldwide tablet market, while China shipped significantly more, 38.4% of the worldwide tablet market by the Chinese white-box vendors only (the last one according to company data and Credit Suisse estimates). This is 5.5% higher than the share of China-based smartphone vendors in the global 2013 smartphone shipments (32.9%, according to DIGITIMES Research—see well below), although in tablet space only Lenovo was a significant player, while in smartphones Huawei, ZTE, Coolpad and TCL were also signicant ones (being actually in the global Top 10). In addition a much higher portion of that was shipped internally: about 50% according to company data and Credit Suisse estimates (as per the “Figure 25” chart in this blog below), while for tablets 3M local brand tablets were shipped (as per Analysys International, see the above chart) against 98M of white-box tablets only (as per company data and Credit Suisse estimates), i.e. around 3%. Even taking the DIGITIMES Research’ 54.4M white-box tablet shipment data as the basis, this number will only climb to around 5.5%.

Note that the 2013 tablet market in China was 17.2M as per the above data, while the 2013 worldwide tablet market was 219.5M per IDC, and 255M according to company data and Credit Suisse estimates (as per the “Figure 30” chart in this blog below). So China was just 7.8% or 6.4% of the worldwide tablet market, while China shipped significantly more, 38.4% of the worldwide tablet market by the Chinese white-box vendors only (the last one according to company data and Credit Suisse estimates). This is 5.5% higher than the share of China-based smartphone vendors in the global 2013 smartphone shipments (32.9%, according to DIGITIMES Research—see well below), although in tablet space only Lenovo was a significant player, while in smartphones Huawei, ZTE, Coolpad and TCL were also signicant ones (being actually in the global Top 10). In addition a much higher portion of that was shipped internally: about 50% according to company data and Credit Suisse estimates (as per the “Figure 25” chart in this blog below), while for tablets 3M local brand tablets were shipped (as per Analysys International, see the above chart) against 98M of white-box tablets only (as per company data and Credit Suisse estimates), i.e. around 3%. Even taking the DIGITIMES Research’ 54.4M white-box tablet shipment data as the basis, this number will only climb to around 5.5%.

Then I need to add here some external analysis as well, for both the smartphone and tablet markets:

From Taiwan Display IC Sector [Credit Suisse Equity research, March 12, 2014]

[p. 10] … We are … seeing entry level tablet shifting from 7″ to 8″ with higher resolutions given the competition from large size smartphone (Phablet). Tablet brands also plan to introduce over 10″ models for more commercial applications. …

China smartphone will continue to proliferate

Credit Suisse Global Research team estimates global smartphone shipment growth of 18% CAGR in 2013-2016E, while China build smartphone shipment (domestic and export) will see 29% CAGR in 2013-16E. For 2014, we forecast total China smartphone DDI [Display Driver IC] demand of 650-700mn units, up 33-36% YoY, and panel resolution to see faster migration on aggressive pricing and less capacity constraint …

[p. 10] Tablet unit demand still solid in 2014 post strong 2013

Tablet set shipment growth is expected to slow down in 2014 (34% YoY) after a strong 57% YoY growth in 2013 and 107% YoY growth in 2012. However, we believe Chinese tablet makers (brand and whitebox) … will outgrow the industry thanks to further cost reduction …

[p. 11] We estimate there will be limited growth for high-end or branded tablets in 2014, with the exception of Samsung (60% YoY growth). We believe the overall tablet demand will be driven by the Chinese, such as Lenovo and whitebox makers.

[2011: 73M*, 2012: 163M, 2013: 255M, 2014E: 342M]

* Samsung’s own data: 2010: 1.5M, 2011: 5.8M, 2012: 16.6M

** Note that the white-box tablet shipments were estimated by DIGITIMES Research as lower: 2012: 54.4M (vs. 58M here), 2013: 89.1M (vs. 98M here)

(as per the 1st chart in this blog above)

2014 China smartphone market and industry – Forecast and analysis [DIGITIMES Research, March 24, 2014]

Digitimes Research expects demand in the domestic China market to reach 422 million smartphones in 2014, with 278 million units contributed by China-based smartphone vendors. The continued expansion by international vendors Samsung and Apple will push up their sales to almost 144 million units, accounting for nearly 4% growth from 2013. As competition in the local market heats up, China-based vendors are turning to overseas markets in order to maintain their shipment volumes, especially taking an aggressive approach to penetrating emerging markets, which hold higher barriers for overseas vendors to enter.

The outlook for the 2014 China domestic smartphone market is that fewer local brands will remain to compete in the market. With the general enhancement of software-hardware specifications in 2013, brand-building and channel management have become the key to sustainability. Vendors without the advantage of substantial product differentiation will face the challenge of being eliminated in the short term. On the other hand, local vendors need to deal with inventories with discretion to counter the vigorous attacks initiated by international vendors in the domestic market.

In terms of the China smartphone industry, Digitimes Research expects global shipments of China-based smartphone vendors to reach 412 million units in 2014, a 30.7% increase from 2013. Overseas shipments will account for about 126 million units. While shipments to mature markets are expected to grow on a small scale, shipments to emerging markets are expected to expand at strong rates, mainly due to the low base they are starting from.

In the forecast for shipments from different vendors in 2014, Lenovo and Huawei are expected to reach 50 million units. Huawei has been engaged in overseas markets for a long time so its export portion outweighs Lenovo’s. ZTE’s and CoolPad‘s shipments are expected to reach 35.5 million units. TCL [Alcatel] has shown a significant growth in exports with shipments expected to exceed 26 million units in 2014, ranking No. 5 on the list. Second-tier vendors Gionee and Xiaomi are expected to ship 20 million units.

Digitimes Research: China smartphone shipments to decline slightly in 1Q14 [DIGITIMES Research, Feb 7, 2014]

China-based handset companies are expected to see their shipments of smartphones decline lightly in the first quarter of 2014, after combined shipments posted a 13% sequential growth in the previous quarter, according to Digitimes Research.

Efforts by brand vendors to clear out entry-level models in previous quarters and increased overseas shipments by Huawei, ZTE and TCL contributed to shipment gains the fourth quarter of 2013.

Additionally, first- and second-tier vendors also launched a number of new models in the fourth quarter to meet demand during the year-end buying season, ramping up total shipments in the quarter.

For all of 2013, China-based handset makers shipped a total of 314 million smartphones, increasing 62.4% from a year earlier, Digitimes Research said.

Second-tier vendors, including Xiaomi Technology, TCL, Oppo Mobile and Gionee managed to ship over 15 million smartphones in 2013.

Digitimes Research: Global smartphone shipments to top 1.24 billion units in 2014 [DIGITIMES Research, Jan 14, 2014]

Global smartphone shipments are expected to top 1.24 billion units in 2014, with Samsung Electronics, Apple, LG Electronics, Sony Mobile Communications, Lenovo, Huawei, Microsoft, ZTE, Coolpad and TCL serving as top-10 vendors, according to Digitimes Research.

Apple may see its shipments double in 2014 largely due to increased shipments to China and Japan as it will benefit from its cooperation with the largest telecom operators in the two countries, said Digitimes Research.

The growth rate for Samsung will be limited in 2014 as its sales in the US, China and Japan will be depressed by growing popularity of iPhones.

China-based Lenovo, Huawei and Coolpad are expected to step up their efforts to boost sales in overseas markets after being enlisted among the top-10 vendors due to higher shipment volumes in the home market in China.

However, TCL and ZTE will continue to ship smartphones to overseas markets mainly, but will also strengthen sales in China, with domestic sales to account for less than 50% of their total shipments in 2014, commented Digitimes Research.

2014 global smartphone market forecast [DIGITIMES Research, Jan 7, 2014]

In 2014, smartphones are expected to continue penetrating rapidly into emerging markets such as Russia, India, Indonesia and Latin America, while China’s smartphone shipments will see weakened on-year growth in the year, but still enormous volume. This report will provide in-depth analyses to forecast whether global smartphone shipments in 2014 will maintain a growth similar to that of 2013 and what the global shipment scale will reach in 2014.

Within the top-10 smartphone vendors in 2013, four of them are from China and in 2014 more China-based vendors are expected to enter the top 10. This report will also analyze which China-based vendors will have the best chance to become parts of the top-tier players.

How Microsoft’s acquisition of Nokia’s handset business will affect Windows Phone products’ shipment growth in 2014 and shake Android and iOS’ domination in the smartphone market, as well as the possibility of Amazon and Facebook joining the smartphone competition in 2014 and their potential influence to the market will also be analyzed within the report.

Digitimes Research: Global smartphone shipments to reach 1.24 billion in 2014 [DIGITIMES Research, Nov 25, 2013]

Global smartphone shipments are expected to reach about 1.24 billion in 2014, up 30% on year [i.e. 954M in 2013], according to Digitimes Research.

The increase in growth is expected to be driven by demand in Russia, India, Indonesia and Latin America countries.

Digitimes Research believes that Samsung Electronics will lead the way in shipments followed by Apple, LG Electronics, Sony, Lenovo, Huawei Device, Microsoft, ZTE, Coolpad and TCL [Alcatel].

Android and IOS operating systems are expected to be used in about 93% of the devices shipped in 2014, added Digitimes Research.

Global tablet market – 4Q 2013 [DIGITIMES Research, March 24, 2014]

Global tablet shipments grew 25% sequentially and 29.8% on year to reach 78.45 million units in the fourth quarter of 2013 benefiting mainly by economic recoveries of Europe and North America, which relatively boosted demand during the year-end holidays.

Digitimes Research: Global tablet shipments in 1Q14 to drop over 20% sequentially [DIGITIMES Research, Jan 27, 2014]

An estimated 62.14 million tablets will ship globally in the first quarter of 2014, decreasing 20.8% on quarter but increasing 10.9% on year, according to Digitimes Research.

iPads will account for 29% of shipments, brand models launched by vendors other than Apple for 36.7%, and models launched by white-box vendors for 34.3%, Digitimes Research indicated.

Of brand tablet shipments in particular, Android-based models will take up 50.5%, iOS-based 44.1% and Windows-based 5.4%. 7.9-inch models will account for 24.8% of the shipments, followed by 7-inch models with 20.2%, 9-inch models with 19.6%, 10-inch models with 18.3% and 8-inch models with 15.3%. In terms of touch solutions, GFF will account for 47.8% of shipments, GF2 for 42.9%, OGS for 5.3%, GG for 2.7% and G1F for 1.3%.

Among vendors, Apple will have the largest global market share at 29%, followed by Samsung Electronics with 23.1%, Lenovo 4.7%, Asustek Computer 2.7%, Amazon 1%, Acer 1%, Microsoft 0.9%, Dell 0.8%, Google 0.5% and Hewlett-Packard 0.5%.

Taiwan-based ODMs/OEMs will ship 22.5 million tablets in the quarter, taking up 55.1% of total brand model shipments. Foxconn Electronics will account for 51.7% of shipments, Pegatron 34.8%, Compal Electronics 5.1%, Wistron 4.3% and Quanta Computer 4.1%.

Digitimes Research: Global tablet shipments in 4Q13 estimated at 78.45 million units [DIGITIMES Research, Jan 24, 2014]

There were an estimated 78.45 million tablets shipped globally in the fourth quarter of 2013, increasing 25% on quarter and by 29.8% on year, according to Digitimes Research.

iPads accounted for 29.7% of shipments, brand models launched by vendors other than Apple for 36.6%, and models launched by white-box vendors for 33.8%, Digitimes Research indicated. Android-based models took up 51.2% of the shipments, iOS-based 44.9% and Windows-based 3.9%. 7-inch models accounted for 31% of the shipments, followed by 9-inch models with 25.4%, 7.9-inch models with 19.7%, 10-inch models with 15.8% and 8-inch models with 7.6%. In terms of touch solutions, GF2 accounted for 41.5% of shipments, GFF for 38.6%, OGS for 9.8% and GG for 9.5%.

Among vendors, Apple had the largest global market share at 29.7%, followed by Samsung Electronics with 17.4%, Amazon 5.4%, Lenovo 4.2%, Asustek Computer 2.8%, Google 1.4%, Acer 1%, Dell 0.8% and Hewlett-Packard 0.5%.

Taiwan-based ODMs/OEMs shipped 32.8 million tablets in the fourth quarter, with Foxconn Electronics accounting for 52.7%, Pegatron 24.4%, Compal Electronics 12%, Quanta Computer 6.6% and Wistron 4.2%.

II. Asia is following different patterns of mobile use than the United States – the case of China and South Korea

The Post-PC Era: Is the U.S. losing its grip on the software industry? [Flurry Blog, Aug 29, 2013]

Just five years ago, PCs reigned supreme and so did the US software industry. In 2008, U.S. companies produced an estimated 65% of all PC software units sold on a worldwide basis.

In only half a decade, smartphones, tablets, and perhaps most importantly, apps, have changed the nature of the software industry. In this post we look at where apps are being developed and used and discuss the implications of that for the Post-PC Era software industry.

More Apps Are Now Being Created Outside The U.S. Than Inside The U.S.

… By June of this year only 36% of the apps we measure were made in the U.S.A. …

…

U.S. Made Apps Still Dominate App Engagement, But Their Share Is Slipping

Of course, some apps enjoy much greater use than others, so we next considered how the picture changes if apps are weighted by total time, which takes into account both user numbers and engagement. Once time is taken into account, things look considerably better for the U.S., suggesting that, on average, user numbers or engagement are greater for apps made in the U.S. than for apps created elsewhere. That makes sense given the size of the U.S. population, the fact that it was an app pioneer country, and the number of English speakers in other countries who might be able to use U.S.-made apps without any localization. Nonetheless, even the weighted percentage of apps made in the U.S.A. has dropped in the past year.

Use of Local Apps Is Strong In China

This should not lull U.S. app developers into a false sense of security however. That becomes evident from examining where the apps used by people in particular countries are made. That’s what the chart below does, starting with the United States. Nearly sixty percent (59%) of the time U.S. users spend in apps is spent in apps developed domestically, meaning that more than 40% of the app time of U.S. consumers is already spent in apps developed in other countries.

And while U.S. made apps are used elsewhere, unsurprisingly, people in many other countries spend a significant amount of their app time in apps developed in their home countries. For example, 13% of the time spent in apps in the UK is spent in apps made in the UK and 8% of the time spent in apps in Brazil is spent in apps made in Brazil. But as is so often the case, it’s China where things get really interesting. Nearly two-thirds of the time spent in apps in China is spent in apps made in China. U.S. made apps only account for 16% of total time spent in apps in China. The size and growth rate of the Chinese app market imply that the worldwide share of time spent in apps that are produced in the U.S. can be expected to contract further.

China Report: Device and App Trends in the #1 Mobile Market [Flurry Blog, July 23, 2013]

In June of this year Flurry Analytics measured 261,333,271 active smartphones and tablets in China. That represented a whopping 24% of the entire worldwide connected device installed base measured by Flurry.

…

Smartphones and tablets are not just about fun and games in China. Compared to iOS device owners elsewhere, the average time Chinese owners spend using Books, Newsstand, Utility, and Productivity apps is greater than the rest of the world (1.8x, 1.7x, 2.3x, and 2.1x respectively). On average Chinese owners of Android devices spend more than seven times as much time in Finance apps (7.4x) than Android owners elsewhere spend in Finance apps, but they also spend more time in Entertainment apps (1.7x).

The South Korea Report: Device and App Trends in The First Saturated Device Market [Flurry Blog, Oct 14, 2013]

In August of this year Flurry Analytics measured 33,527,534 active smartphones and tablets in South Korea. While that was only 2.8% of the entire worldwide connected device installed base Flurry measures, South Korea is an important market for connected devices for several reasons. First, it is the first connected device market in the world to approach saturation. Second, it is Samsung’s home market, and largely as a consequence of that, more of the devices in use there are manufactured by domestic firms than is the case for any other country. Finally, it is home to more phablet fans than anywhere else.

…Social networking accounts for a significant share of app activity in South Korea, as it does in many other countries. Tool apps are used heavily by South Korean Android users, and entertainment apps capture a lot of time spent in iOS apps.

Compared to app users elsewhere, South Koreans over-index on Entertainment apps on iOS and several Android app categories (Media / Video, Photography, Lifestyle, Shopping, and Tools).

…

Given that South Korea’s rapid period of connected device growth was ushered in by the phablet, it is perhaps not surprising that it continues to surpass the rest of the world in its preference for that form factor. As shown below, in a worldwide sample of 97,963 iOS and Android devices, only 7% were phablets, but for South Korea that percentage was 41%. The appeal of phablets in South Korea appears to suppress the tablet market there. Worldwide, 19% of the devices in our sample were tablets compared to only 5% in South Korea.

Worldwide:

Size Matters for Connected Devices. Phablets Don’t. [Flurry Blog, April 1, 2013]

… For this study, we focused on the top 200 device models, as measured by active users in Flurry’s system, which represent more than 80% of all usage. Doing so, five groups emerged based on screen size:

1. Small phones (e.g., most Blackberries), 3.5” or under screens

2. Medium phones (e.g., iPhone), between 3.5” – 4.9” screens

3. Phablets (e.g., Galaxy Note), 5.0” – 6.9” screens

4. Small Tablets (e.g., Kindle Fire), 7.0” – 8.4” screens

5. Full-size tablets (e.g., the iPad), 8.5” or greater screens

…

The ‘Is it a phone or is it a tablet’ devices otherwise known as phablets have attracted interest, but currently command a relatively small share (2%) of the device installed base, and their share of active users and sessions is also relatively small.

…

Android owns the phablet market and also has the greatest proportion of devices using small tablets. iOS has the greatest share of active devices using large tablets.

…

… notice that nearly a third of time spent playing games take places on larger devices, namely full-sized tablet, small tablets and phablets. And while they command consumer time spent, they represented only 15% of device models in use in February and 21% of individual connected devices. These differences are statistically significant.Studying books and videos, it’s somewhat surprising that tablets, which possess larger screens, do not see a larger proportion of time spent. An explanation for the high concentration in time spent in smartphones could be that consumers watch videos from their smartphones on-the-go (e.g., commuting to work on public transit), whereas they opt for a bigger screen to watch video (e.g., computer or TV) when at work or home. We expect that tablets may represent a greater share of time spent in book and video apps in the future as tablet ownership expands and tablet owners branch out into more types of apps.

…

From our study, consumers most prefer and use apps on medium-sized smartphones such as the Samsung Galaxy smartphones and full-sized tablets like the iPad. In particular, smaller smartphones under-index in terms of app usage compared to the proportion of the installed base they represent, and would suggest they are not worth developers’ support.

…

Mobile Use Grows 115% in 2013, Propelled by Messaging Apps [Flurry Blog, Jan 13, 2014]

… the segment that showed the most dramatic growth [worldwide] in 2013 was Messaging (Social and Photo sharing included). The growth in that segment should not come as a surprise to many, given the attention that messaging apps such as WhatsApp, WeChat, KakaoTalk, LINE, Facebook Messenger and SnapChat have received in the press. What is surprising, however, is that the rate of growth (tripling usage year-over-year) dramatically outpaced other popular categories. This type of growth could explain the high valuation Facebook has allegedly put on SnapChat, or Facebook’s rush to add direct messaging in Instagram, an app frequented by teens.

…

Another explosive growth year in mobile has passed. On December 31st, 2013 at 11:59 pm, Flurry Analytics tracked a record 4.7 Billion app sessions in a single day, for a total of 1.126 Trillion sessions for the whole year. Those are some very, very big numbers. …

The Truth About Cats and Dogs: Smartphone vs Tablet Usage Differences [Flurry Blog, Oct 29, 2012]

… Taking a snapshot in September 2012 from Flurry Analytics, that totaled more than 6 billion application sessions across approximately 500 million smart devices, Flurry provides a comprehensive comparison between smartphones and tablets, spanning age, gender, time of day usage, category usage and engagement metrics. For age and gender comparisons, Flurry leverages a panel of more than 30 million consumers who have opted-in to share demographic data. …

…

The chart below compares the time spent across app categories between smartphones and tablets. At a high level, consumers spend more time using tablets for media and entertainment, including Games (67%), Entertainment (9%) and News (2%) categories which account for nearly four-fifths of consumption on tablets. Smartphones claim a higher proportion of communication and task-oriented activities with Social Networking (24%), Utilities (17%), Health & Fitness (3%) and Lifestyle (3%) commanding nearly half of all usage on smartphones. Games are the most popular category on both form factors with 67% of time spent using games on tablets and 39% of time spent using games on smartphones. Further reinforcing that tablets are “media machines” is the fact that consumers spend 71% more of their time using games on tablets than they spend doing so on smartphones.

Indie Game Makers Dominate iOS and Android [Flurry Blog, March 6, 2012]

For the first two months of 2012, Flurry Analytics measured that more than half of all end user sessions were spent in games. Across January and February, Flurry observed sessions across a sample of more than 64 billion applications sessions across more than 500 million iOS and Android devices.

United States

:

Apps Solidify Leadership Six Years into the Mobile Revolution [Flurry Blog, April 1, 2014]

Last year, on the eve of the fifth anniversary of the mobile revolution, Flurry issued its five-year report on the mobile industry. In that report we analyzed time-spent on mobile devices by the average US consumer. We have run the same analysis, using data collected between January and March of 2014, and found some interesting shifts that we are sharing in this report

…The chart

belowon the left takes a closer look at app categories. Comparing them to last year, gaming apps maintained their leadership position at 32% of time spent. Social and messaging applications, including Facebook, increased share from 24% to 28%. Entertainement (including YouTube) and Utility applications maintained their positions at 8% each, while productivity apps saw their share double from 2% to 4% of the overall time spent.

Flurry Five-Year Report: It’s an App World. The Web Just Lives in It

[Flurry Blog, April 3, 2013]

… On the five-year anniversary of launching Flurry Analytics, we took some time to reflect on the industry and share some insights. First, we studied the time U.S. consumers spend between mobile apps and mobile browsers, as well as within mobile app categories. Let’s take a look. …

Mobile App Usage [in U.S.] Further Dominates Web, Spurred by Facebook [Flurry Blog, Jan 9, 2012]

The chart compares how daily interactive consumption has changed over the last 18 months between the web (both desktop and mobile web) and mobile native apps. For the web, shown in green, we built a model using publicly available data from comScore and Alexa. For mobile application usage, shown in blue, we used Flurry Analytics data, which tracks anonymous sessions across more than 140,000 applications. We estimate this accounts for approximately one third of all mobile application activity, which we scaled-up accordingly for this analysis.

…

With mobile app usage soaring, Flurry additionally studied which categories most occupy consumers’ time. The results are shown in the pie chart below.

Further considering that Flurry does not track Facebook usage, the Social Networking category is actually larger. Combined, from just what Flurry can see, these two categories control a whopping 79% of consumers’ total app time. This breakdown in usage reveals Facebook’s inherent popularity as the leading social network, as well as how important controlling the game category is for all platform providers. As we drill down into the category data, consumers use these two categories more frequently, and for longer average session lengths, compared to other categories.

Chinese smartphone brands to conquer the global market?

The smartphone market in China became saturated between Q3’12 and Q4’13 as per the below chart from Analysys International (EnfoDesk):

Note that this chart corresponds to Chinese writing traditions, i.e. in Q2’11 16.81 million smartphones and 51.01 million feature phones were sold, while in Q4’13 97.63 million smartphones and 9.2 million feature phones. Source: 易观分析:2013年第4季度中国手机销量增速放缓,智能手机市场呈现饱和态势 (Analysys analysis: China mobile phone sales growth slowed in the fourth quarter of 2013, the smart phone market is saturated) [EnfoDesk, March 11, 2014]

Chinese Handset Vendors Will Account for Over 50% of Mobile Handset Sales in 2015 [ABI Research press release, March 10, 2014]

ABI Research reports that Chinese handset vendors will account for over 50% of mobile handsets in 2015. Chinese vendors already accounted for 38% of mobile handset shipments in 2013 and the ongoing shift in growth to low cost handsets, especially smartphones, will increase their market share.

Greater China has long dominated the mobile handset manufacturing supply chain, but now its OEMs are beginning to dominate sales at the expense of the traditional handset OEMs, including even Samsung.

Many of the Chinese OEMs have focused almost exclusively on the huge Chinese market, with little activity beyond its borders, but this is set to change. Huawei (6th in worldwide market share for 2013) and ZTE (5th) have already made an impact on the world stage, but other Chinese handset OEMs like Lenovo—the Motorola acquisition is a clear statement of intent—and Xiaomi are set to join them.

“Chinese vendors already take up five of the top ten places in terms of worldwide market share, despite three of them only really shipping into China. The Chinese vendors highlight the changing shape of the mobile handset market, as the Chinese manufacturing ecosystem, specifically reference designs, enable the next wave of smartphone growth in low cost emerging markets and amongst price conscious consumers everywhere,” said Nick Spencer, senior practice director, mobile devices.

“South East Asia has already experienced this trend, but ABI Research expects to see the impact of these Chinese vendors increasing in all emerging markets and even advanced markets, especially on prepay,” added Spencer.

The New Phone Giants: Indian And Chinese Manufacturers’ Fast Rise To Threaten Apple And Samsung [Business Insider India, March 15, 2014]

The top Indian and Chinese smartphone manufacturers are classically disruptive. They produce products that are “good enough,” at a fraction of the cost of comparable models from premium brands. These ultra low-cost devices are the key to nudging consumers in massively untapped markets like India and Indonesia onto smartphones.

And these companies are starting to aim higher – producing 4G LTE smartphones that have the same processing power as Samsung and Apple premium devices.

They’re also far more innovative than they’re given credit for in terms of their strategy, supply chain management, and hardware.

In a new report from BI Intelligence, we explain why global consumer Internet and mobile companies will increasingly need to work with companies like Xiaomi and Micromax – not to mention Lenovo, Huawei, ZTE, Coolpad, Karbonn, and others – if they don’t want to miss out on mobile’s next growth phase in emerging markets

- Major local manufacturers now account for two-fifths of China’s smartphone market, and one-fourth of India’s. Xiaomi already sells four of the top 10 best-selling Android devices in China, and operates one of the top five app stores.

- Combined, the top five manufacturers in China and the top two in India – the “Local 7” in the chart above – are now shipping about 65 million smartphones every quarter, more than Apple, and coming close to drawing even with Samsung.

- These local manufacturers wield influence in various ways. They run their own successful app stores, mobile operating systems, and mobile services. They also hold the keys to which apps are preloaded on their phones. When BlackBerry wanted to take its BBM messaging service for Android into India, it signed a deal with Micromax.

- The local manufacturers are not provincial outfits producing knock-offs, as some might be inclined to assume. But their main competitive tool, for now, remains price. Local manufacturers in China and India match the features of more expensive devices and manage to produce comparable hardware at a fraction of the price. A Micromax handset comparable to Apple’s iPhone 5C costs less than one-fourth as much.

- Xiaomi has used a four-point strategy in its three-year rise to produce four of the most popular phone models in China. We discuss all four aspects, including tight inventory management and crowdsourcing product development feedback.

- These manufacturers will continue to expand overseas, in search of new growth opportunities. Micromax is in Nepal, Bangladesh, and Sri Lanka. Xiaomi has its eyes on Malaysia and Brazil. Huawei is already in the U.S. For example, it sells a 4G LTE handset on MetroPCS.

Smartphone Prices Race to the Bottom as Emerging Markets Outside of China Come into the Spotlight for Future Growth, According to IDC [press release, Feb 24, 2014]

Singapore and London, February 24, 2014 – Emerging markets have become the center of attention when talking about present and future smartphone growth. According to the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker, in 2013 the worldwide smartphone market surpassed 1 billion units shipped, up from 752 million in 2012. This boom has been mainly powered by the China market, which has tripled in size over the last three years. China accounted for one out of every three smartphones shipped around the world in 2013, equaling 351 million units.

Recently the surge in growth has started to slow as smartphones already account for over 80% of China’s total phone sales. The next half billion new smartphone customers will increasingly come mainly from poorer emerging markets, notably India and in Africa.

“The China boom is now slowing,” said Melissa Chau, Senior Research Manager for mobile devices at IDC Asia/Pacific. “China is becoming like more mature markets in North America and Western Europe, where smartphone sales growth is slackening off.”

Emerging markets in Asia/Pacific outside of China, together with the Middle East and Africa, Central and Eastern Europe, and Latin America, account for four fifths of the global feature phone market, according to IDC data. “This is a very big market opportunity,” said Simon Baker, Program Manager for mobile phones at IDC CEMA. “Some 660 million feature phones were shipped last year, which could add two thirds to the size of the current global smartphone market.”

India will be key to future smartphone growth as it represents more than a quarter of the global feature phone market. “Growth in the India market doesn’t rely on high-end devices like the iPhone, but in low-cost Android phones. Nearly half of the smartphones shipped in India in 2013 cost less than US$120,” said Kiranjeet Kaur, Senior Market Analyst for mobile phones at IDC Asia/Pacific.

“Converting feature phone sales to smartphone sales implies a relentless push towards low cost,” added Baker. IDC research shows nearly half the mobile handsets sold across the world have retail prices of less than US$100 without sales tax. Two thirds of those have prices of less than US$50.

“The opportunity gets larger the lower the price falls,” continued Baker. “If you take retail prices without sales tax, in 2013 nearly three quarters of the US$100-125 price tier was already accounted for by smartphones. Within US$75-100 the proportion was down to just over half, and between $50-75 it was not much more than a third.”

Many smartphone vendors have begun gearing up for this next wave of cost pressure. Samsung is increasingly switching production to Vietnam, where manufacturing costs currently undercut mainland China. Even Hon Hai, one of the largest contract manufacturers for handsets in China, has announced plans for a plant in Indonesia to furnish a lower production cost base.

In addition to the table below, an interactive graphic showing worldwide sub-$100 feature phone shipments by region is available here. The chart is intended for public use in online news articles and social media. Instructions on how to embed this graphic can be found by viewing this press release on IDC.com.

Worldwide Sub-$100 Feature Phone Shipments by Region, 2013

Region

Shipments (M Units)

India

212.3

Middle East & Africa

150.0

Asia/Pacific (excluding Japan, China, and India)

140.7

Latin America

76.4

PRC

68.1

Central & Eastern Europe

43.6

Western Europe

39.8

North America

13.9

Total

744.9

Source: IDC Worldwide Mobile Phone Tracker, February 24, 2014

Analysys International: Xiaomi Ranked Among Top Five in Q4, 2013 [March 11, 2014]

The statistics from EnfoDesk, the Survey of China Mobile Terminals Market in Q4, 2013, newly released by Analysys International, shows that the market share of Samsung, Lenovo, Huawei, Coolpad and Xiaomi ranked the top five of China smartphone in Q4, 2013. The market share of Samsung shrink slightly over the previous quarter, but it still accounted for 15.07 percent of smartphone market and maintain the leading position.

The release of Apple‘s new product has brought efficiency in Q4, and its market share slightly rebounded. Owning to the release of MI3 (Xiaomi), the market share of Xiaomi up 3.85 percentage points compared to the previous quarter. MI3 still should be bought from booking and the booking is relatively frequent. Meanwhile, the purchase restriction of MI2(Xiaomi) and Red MI(Xiaomi) has been relaxed, coupled with the strategic cooperation between Xiaomi and mobile operators, making it easier to buy custom models as well as contributing to the enlargement of Xiaomi’s market share. It can be expected that Xiaomi will put more energy into the complement of its retail capabilities and continue to increase their market share.

From: UMENG Insight Report – China Mobile Internet 2013 Overview [UMENG, March 12, 2014]

– The number of active smart devices in China exceeded 700 Million by the end of 2013.

– The five fastest growing mobile apps categories (excluding games) are : news, health & fitness, social networking, business, and navigation. These areas will bring new opportunities for developers in 2014.

– Socializing your apps is the key to success for developers. Currently among the top 1,000 apps (apps and games) in the Chinese market, 55% of them provide links to Chinese social networking services (e.g. Sina Weibo, Wechat, QQ, Renren) The amount of app content sharing to social network platforms per mobile Internet user per day has tripled in the last 6 months.

– Social network sharing in game has become incredibly popular on all social networking platforms, 48% of in app sharing traffic to social networks are from games.

– High-end devices (pricing above 500US$) have a significant market share in China, contributing 27% of total devices. These users have dynamic needs on mobile apps . The users of below 150US$ phones prefer casual games for their entertainment requirements.

– The year of 2013 became known as the first year Chinese developers took IP seriously with many developers licensing IP from rights holders. By the end of 2013, among the Top 100 games, 20% license 3rd party IP.