Home » Posts tagged 'iOS'

Tag Archives: iOS

Tablet and smartphone market trends

September update: Qualcomm’s smartphone AP revenues declined 17% year-over-year in the second quarter of 2015, Strategy Analytics estimated. Qualcomm maintained its smartphone AP market share leadership with 45% revenue share, followed by Apple with 19% revenue share and MediaTek with 18% revenue share. For the rest 18%: After a difficult 2014, Samsung LSI continued to recover and more than doubled its smartphone AP shipments in the second quarter of 2015 compared to the same period last year. Samsung LSI capitalised on its Galaxy S6 design-win in Q2 2015. In addition the company featured in multiple mid-range smartphones from Samsung Mobile. Full report: Smartphone Apps Processor Market Share Q2 2015: Samsung LSI Maintains Momentum

… The global tablet AP market declined 28% year-over-year to reach US$679 million in the second quarter of 2015, according to Strategy Analytics. Apple, Intel, Qualcomm, MediaTek and Samsung LSI captured the top-five revenue share rankings in the market during the quarter. Apple led the tablet AP market with 27% revenue share, followed by Intel with 18% revenue share. Qualcomm ranked number three, narrowly behind Intel. ![GT400150821[1]](https://lazure2.wordpress.com/wp-content/uploads/2015/08/gt4001508211.jpg?w=960) Full report: Tablet Apps Processor Market Share Q2 2015: Apple and Intel Maintain Top Two Spots

Full report: Tablet Apps Processor Market Share Q2 2015: Apple and Intel Maintain Top Two Spots

…

Digitimes Research saw global tablet shipments fall to 45.76 million units in second-quarter 2015, showing a 10% decrease on quarter and representing more than a 15% decrease on year. Full report: Global tablet market – 2Q 2015 End of September update

Investors.com comments on tablet and smartphone market trends — Q2’2015: 1. Apple, Samsung lose ground in tablet market — LG and Huawei gain

1. Apple, Samsung lose ground in tablet market — LG and Huawei gain

2. Apple, Huawei [and Xiaomi] buck slowing smartphone sales trend

As the commenting articles by Investors.com are based on press releases of 2 market research companies I will give the web reference here for those press releases themselves, as well as 3 other press releases not commented on by Investors.com (if there are trend indications in the press releases themselves I will copy them alongside the web reference):

- July 29, 2015: Worldwide Tablet Market Continues to Decline; Vendor Landscape is Evolving, According to IDC

“Longer life cycles, increased competition from other categories such as larger smartphones, combined with the fact that end users can install the latest operating systems on their older tablets has stifled the initial enthusiasm for these devices in the consumer market,” said Jitesh Ubrani, Senior Research Analyst, Worldwide Mobile Device Trackers. “But with newer form factors like 2-in-1s, and added productivity-enabling features like those highlighted in iOS9, vendors should be able to bring new vitality to a market that has lost its momentum.”

“Longer life cycles, increased competition from other categories such as larger smartphones, combined with the fact that end users can install the latest operating systems on their older tablets has stifled the initial enthusiasm for these devices in the consumer market,” said Jitesh Ubrani, Senior Research Analyst, Worldwide Mobile Device Trackers. “But with newer form factors like 2-in-1s, and added productivity-enabling features like those highlighted in iOS9, vendors should be able to bring new vitality to a market that has lost its momentum.” - July 30, 2015: Huawei Becomes World’s 3rd Largest Mobile Phone Vendor in Q2 2015 [says Strategy Analytics]

- Woody Oh, Director at Strategy Analytics, said, “… Smartphones accounted for 8 in 10 of total mobile phone shipments during the quarter. The 2 percent growth rate of the overall mobile phone market is the industry’s weakest performance for two years, due to slowing demand for handsets in China, Europe and the US.”

- Neil Mawston, Executive Director at Strategy Analytics, added, “… Samsung has stabilized volumes in the high-end, but its lower-tier mobile phones continue to face intense competition from rivals such as Huawei in Asia. … Apple outperformed as consumers in China and elsewhere upgraded to bigger-screen iPhone 6 and 6 Plus models.”

- Ken Hyers, Director at Strategy Analytics, added, “… Huawei is rising fast in all regions of the world, particularly China where its 4G models, such as the Mate7, are proving wildly popular. Huawei has finally overtaken Microsoft to become the world’s third largest mobile phone vendor for the first time ever.”

- Neil Mawston, Executive Director at Strategy Analytics, added, “Microsoft shipped 27.8 million mobile phones and captured 6 percent marketshare worldwide in the second quarter of 2015. Microsoft’s 6 percent global mobile phone marketshare is sitting near an all-time low. Microsoft continues to lose ground in feature phones, while its Lumia smartphone portfolio is in a holding pattern awaiting the launch of new Windows 10 models later this year. Xiaomi shipped 19.8 million mobile phones and captured 5 percent marketshare worldwide in Q2 2015. Xiaomi remains a major player in the China mobile phone market, but its local and international growth is slowing and Xiaomi is facing intense competition from Huawei, Meizu and others. As a result, Xiaomi may struggle to hold on to its top-five global mobile phone ranking in the coming quarters.”

- June 17, 2015: Business smartphones shipments in Q1 up 26% from last year, now 27% of total smartphone market [says Strategy Analytics]

Android was the most dominant OS in terms of business smartphone shipments in Q1, accounting for nearly 60% of all business smartphones (corporate- and personal-liable). It was also the dominant BYOD device; 68% of personal-liable shipments in Q1 were Android. Apple iOS accounted for only 27% of BYOD shipments in Q1, but was the dominant platform in terms of corporate-liable smartphones, with 48% of Q1 CL shipments. The difference in Android/iOS shipments between the CL and IL categories reflects the continuing corporate perception that iPhones are “safer” than Android-based devices.

Android was the most dominant OS in terms of business smartphone shipments in Q1, accounting for nearly 60% of all business smartphones (corporate- and personal-liable). It was also the dominant BYOD device; 68% of personal-liable shipments in Q1 were Android. Apple iOS accounted for only 27% of BYOD shipments in Q1, but was the dominant platform in terms of corporate-liable smartphones, with 48% of Q1 CL shipments. The difference in Android/iOS shipments between the CL and IL categories reflects the continuing corporate perception that iPhones are “safer” than Android-based devices.

- Shipments of personal-liable smartphones (i.e. “bring your own device,” or BYOD, phones) drove market growth in Q1

- Strategy analytics defines personal-liable devices as devices purchased by the end-user and expensed back to the company or organization, or devices purchased outright by individual users but used primarily for business purposes linking to corporate applications and backend systems.

- While personal liable devices dominate worldwide business smartphone shipments, some regions are more resistant to the BYOD trend than others. Such regions include Western Europe and Central Europe, where corporate-liable devices are the dominant types of business smartphones. In Western Europe in Q1, 61% of the 10 million business smart phones were corporate-liable. Central and Eastern Europe had a slightly higher rate of BYOD devices shipped in Q1 — 41% — but the majority of smartphones shipped in this regions was also corporate-liable. This a sharp contrast to North America, where three-quarters of business smartphone shipments are personal-liable. The trend in Western and Eastern Europe reflects the more corporate-centric approach businesses take to mobility in these regions.

- July 29, 2015: Mobile Broadband Tablet Subscriptions to Double to 200 Million by 2021, says Strategy Analytics

- Strategy Analytics forecasts global mobile data subscriptions on tablets will more than double from 2015 to 2021, reaching over 200 million

- Around the globe, over 100 million wireless connections on cellular enabled tablets will be added through 2021. By 2021 tablets will only account for 2 percent of total mobile subscriptions, a 2.7 percent population penetration rate.

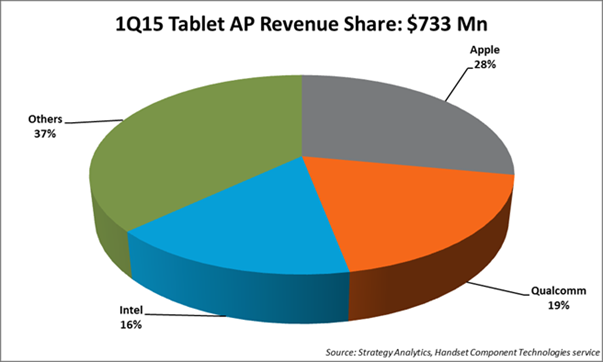

- July 29, 2015: Intel Maintains Top Spot in Non-Apple Tablet Apps Processors in Q1 2015 says Strategy Analytics

⇒The global tablet applications processor (AP) market declined -6 percent year-over-year to reach $733 million in Q1 2015- According to Sravan Kundojjala, Associate Director, “Intel maintained its top spot in the non-Apple tablet AP market in unit terms in Q1 2015. Strategy Analytics estimate Android-based tablets accounted for over 70 percent of Intel’s total tablet AP shipments in Q1 2015. We expect Intel’s Atom X3 cellular tablet chip product line to help Intel maintain its momentum in the tablet AP market.”

- Stuart Robinson, Executive Director of the Strategy Analytics Handset Component Technologies (HCT) service added, “Strategy Analytics estimates that baseband-integrated tablet AP shipments accounted for over one-fourth of total tablet AP shipments in Q1 2015, helped by a strong push from Qualcomm, MediaTek and Spreadtrum. We expect continued momentum for integrated APs as Intel, Rockchip and others join the bandwagon.”

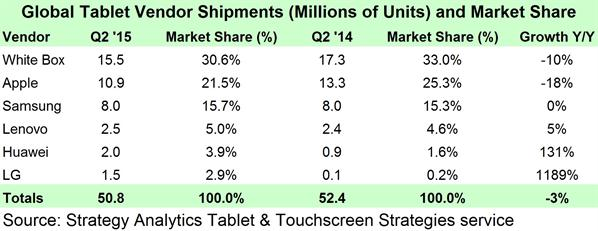

- July 30, 2015: Windows Tablet Shipments Nearly Double in Q2’15, says Strategy Analytics

⇒Global Tablet Shipments and Market Share in Q2 2015 (preliminary)

- Windows-branded Tablets comprised 9 percent of shipments in Q2 2015, up 4 points from Q2 2014

- Android-branded Tablet shipment market share was flat at 70 percent in Q2 2015

- Apple continued its slide in market share down to an all-time low of 21 percent in Q2 2015, 4 points lower than Q2 2014

- Vendors with strong 3G and LTE connected Tablet strategies such as Huawei, LG, and TCL-Alcatel gained market share as leaders like Apple, Samsung, and the White Box community lost ground

Tablet & Touchscreen Strategies Senior Analyst Eric Smith added, “Windows share continues to improve as more models become available from traditional PC vendors, White Label vendors, and Microsoft itself though a healthy Surface lineup and distribution expansion. The key going forward will be if the coming wave of 2-in-1 Detachable Tablets is a hit with consumers or if they go the way of the Netbook—we remain cautiously optimistic on this point.” |

Tablet & Touchscreen Strategies Service Director Peter King said, “Apple’s fortunes will turn around soon as it will launch the 12.9-inch iPad Pro as well as an iPad mini 4 in Q4 2015. New features in iOS 9, which are exclusive to iPad such as multi-tasking and a more convenient soft keyboard, will also help compel upgrades by owners of older iPad models. Meanwhile, Huawei and LG have posted fantastic growth primarily due to well-executed 3G and LTE connected Tablet strategies.” |

Then I will add 2 additional information pieces from Strategy Analytics:

Oct 8, 2014: Replacement Demand to Boost PC Sales in 2015, says Strategy Analytics

Having experienced negative growth since 2012, global PC sales are expected to rise 5 percent in 2015 driven by replacement of an ageing installed base according to Strategy Analytics’ Connected Home Devices (CHD) service report, “Computers in the Post-PC Era: Growth Opportunities and Strategies.”

Click here for the report:

http://www.strategyanalytics.com/default.aspx?mod=reportabstractviewer&a0=10146

- PC sales will fall by 4 percent in 2014 before returning to modest growth in 2015 and beyond to support replacement demand.

- Strategy Analytics’ consumer research of computing device usage in developed markets indicates that PCs remain essential computing devices despite healthy Tablet sales.

- Frequent Tablet usage has grown by 22 percentage points from 2011 to Q4 2013 up to 32 percent of all households while frequent Mobile PC (excluding Tablets) usage has stayed steady through this period, as 63 percent of all households indicated they frequently used Mobile PCs.

- Frequent usage of all PCs (including Mobile and Desktop PCs and excluding Tablets) remained above the 90 percent mark of all households, falling only 3 percentage points during this period.

Quotes:

Eric Smith, Analyst of Connected Home Devices, said: “Multiple PC ownership is falling as Tablet sales supplant replacement demand for secondary PCs mainly used for casual tasks. Still, PCs will remain essential devices as households eventually replace their primary PCs used for productivity tasks such as spreadsheet and video editing or personal banking.”

David Watkins, Service Director, Connected Home Devices, added: “The modern Tablet user experience is quickly arriving on the PC thanks to more affordable 2-in-1 Convertible PCs and new operating systems which blend traditional PC and Tablet user experiences. We see development of these forces aligning perfectly with an older PC installed base ripe for replacement in 2015.”

May 1, 2015: Children Change Disney’s Digital Strategy: “App TV” Now Central To Content Planning by David Mercer

Multiscreen TV behaviour is at the centre of television’s stormy transformation – viewing of broadcast, linear TV on the TV screen is apparently in decline while consumption on smartphones and tablets is increasing. Making sense of the big picture is increasingly challenging, and legacy players like broadcasters and the major content owners are inevitably somewhat resistant to the idea that their traditional businesses are under serious threat.

We have monitored the early stages of this transformation for the past decade and see its results in our own research, and we continue to predict further industry disruption in our forecasts. But sometimes it is only when you hear the evidence given in person by a senior executive at a leading global player that the scale of the challenge and opportunity are finally brought home.

This happened at last week’s AppsWorld event in Berlin, where I chaired the TV and Multiscreen conference. The speaker was Andreas Peters, Head of Digital for the Walt Disney Company Germany, Austria and Switzerland. Andreas presented some of the most compelling evidence I have yet heard that television is truly a multiscreen medium for the next generation of viewers.

Disney’s challenge in Germany was to launch a television show called Violetta aimed at 8-12 year old girls. It had been introduced successfully in Argentina but had failed in the UK. As it often does, Disney had invested considerable amounts in merchandising and retailers were eagerly anticipating sales of the new product lines. The show was first broadcast on German free TV on May 1st 2014 but it achieved only very low ratings.

The question for Disney managers was whether traditional TV had stopped working. A crisis meeting was held with a view to writing off the investment. Disney had previously not made its shows available online in Germany but the Violetta situation was so serious they were persuaded to experiment. Two episodes were made available on Youtube with a link to Disney’s own website. Viewing of the content on Youtube very quickly went viral until Disney had achieved a reach of 50% of 8-12 year old girls and eight million views. Violetta went on to become a success in German-speaking markets.

The evidence was clear: for some shows at least, younger children cannot now be reached using the traditional broadcast TV/big screen model. Peters explained that the Violetta experience was transformative for the Disney organisation and led to the inclusion of online and digital media as a key element in the business case for many products. In fact it also led to the development and launch of Disney’s own Watch App, which includes live streaming and seven-day catch-up programmes from the broadcast Disney Channel.

Even after the Violetta experience Disney was sceptical that an app was needed – there was a feeling that the website would be sufficient. Nevertheless the app was launched and Disney had planned for 20,000 downloads. Instead it has passed one million downloads in its first six months. Peters noted: “This was a real shock for us. We completely underestimated the demand.” Around 500,000 viewers are now using the Disney Watch app for linear television viewing, in addition to millions of shows being downloaded for catch-up viewing. Peak app viewing hours are between 6am and 8am and then between 1pm and 9pm on school days, with a different pattern at weekends. Peters made it clear that children did not want lots of features built in to the app – just like TV, they just want to hit “play” and watch.

“Our TV colleagues of course don’t want to believe this,” said Peters. “But the world has changed and it will continue to change.” Disney has also seen a knock-on effect from its app launch with an increase in free-to-air broadcast TV viewing. But the firm is now clear that mobile is not just an add-on to TV or a promotional tool; it must be an integral part of the entire process.

There are many implications for content strategy. TV and Digital have to “understand each other”, which is a challenge when the KPIs in each world are very different. As we have often heard, the video industry is crying out for a set of common metrics which can apply and support advertisers in both TV and online worlds. Video consumption patterns vary and different content may be relevant to different platforms.

But the overall lesson is clear: “TV” is not just the big screen in the corner of the living room. It must embrace multiscreen distribution strategies in order to reach its maximum potential. TV companies are betraying their audiences and their investors if they don’t target the 6.4bn addressable screens available to them.

2014 H1 changes on the Worldwide Tablet market

Versus as it was presented in The lost U.S. grip on the mobile computing market, including not only the device business, but software development and patterns of use in general [this same blog, April 14, 2014]:

Source: The Tablet Market Ticks Up In The Second Quarter

Source: The Tablet Market Ticks Up In The Second Quarter

With White Box Shipments Leading The Way [Business Insider, July 25, 2014]

-

The global tablet market ticked up in the second quarter of 2014, although growth is still near the market’s historical low.

- Shipments hit about 44.3 million during the period, yielding year-over-year growth of 11%.

While an improvement from the previous quarter, consider that the tablet market had year-over-year growth of nearly 80% in the same quarter just a year ago.

- Although it lead all vendors with about 27% market share, Apple’s iPad shipments declined 9% year-over-year during the period. That marks the second consecutive quarter in which iPad shipments have declined.

- Samsung’s tablet shipments grew a paltry 1% for the period to hit 8.5 million units in the second quarter. That is an enormous slowdown compared to the growth rates it was achieving just a year ago. In the second quarter of 2013, Samsung tablet shipments grew 300% year-over-year.

- Both Apple and Samsung lost market share during the quarter. Apple’s leading market share fell from 33% to 27% while Samsung’s dipped two percentage points to 17%.

- “White-box” vendors = 41% of market

Worldwide Tablet Market Grows 11% in Second Quarter on Shipments from a Wide Range of Vendors, According to IDC [IDC press release, July 24, 2014]

The worldwide tablet grew 11.0% year over year in the second quarter of 2014 (2Q14) with shipments reaching 49.3 million units according to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Tablet Tracker. Although shipments declined sequentially from 1Q14 by -1.5%, IDC believes the market will experience positive but slower growth in 2014 compared to the previous year.

“As we indicated last quarter, the market is still being impacted by the rise of large-screen smartphones and longer than anticipated ownership cycles,” said Jean Philippe Bouchard, IDC Research Director for Tablets. “We can also attribute the market deceleration to slow commercial adoption of tablets. Despite this trend, we believe that stronger commercial demand for tablets in the second half of 2014 will help the market grow and that we will see more enterprise-specific offerings, as illustrated by the Apple and IBM partnership, come to market.”

Despite declining shipments of its iPad product line, Apple managed to maintain its lead in the worldwide tablet market, shipping 13.3 million units in the second quarter. Following a strong first quarter, Samsung struggled to maintain its momentum and saw its market share slip to 17.2% in the second quarter. Lenovo continued to climb the rankings ladder, surpassing ASUS and moving into the third spot in the tablet market, shipping 2.4 million units and grabbing 4.9% markets share. The top 5 was rounded out by ASUS and Acer, with 4.6% and 2.0% share, respectively. Share outside the top 5 grew to an all time high as more and more vendors have made inroads in the tablet space. By now most traditional PC and phone vendors have at least one tablet model in the market, and strategies to move bundled devices and promotional offerings have slowly gained momentum.

“Until recently, Apple, and to a lesser extent Samsung, have been sitting at the top of the market, minimally impacted by the progress from competitors,” said Jitesh Ubrani, Research Analyst, Worldwide Quarterly Tablet Tracker. “Now we are seeing growth amongst the smaller vendors and a levelling of shares across more vendors as the market enters a new phase.”

Worldwide Tablet Shipments Miss Targets as First Quarter Experiences Single-Digit Growth, According to IDC [IDC press release, May 1, 2014]

Worldwide tablet plus 2-in-1 shipments slipped to 50.4 million units in the first calendar quarter of 2014 (1Q14) according to preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Tablet Tracker. The total represents a sequential decline of -35.7% from the high-volume holiday quarter and just 3.9% growth over the same period a year ago. The slowdown was felt across operating systems and screen sizes and likely points to an even more challenging year ahead for the category.

“The rise of large-screen phones and consumers who are holding on to their existing tablets for ever longer periods of time were both contributing factors to a weaker-than-anticipated quarter for tablets and 2-in-1s,” said Tom Mainelli, IDC Program Vice President, Devices and Displays. “In addition, commercial growth has not been robust enough to offset the slowing of consumer shipments.”

Apple maintained its lead in the worldwide tablet plus 2-in-1 market, shipping 16.4 million units. That’s down from 26.0 million units in the previous quarter and well below its total of 19.5 million units in the first quarter of 2013. Despite the contraction, the company saw its share of the market slip only modestly to 32.5%, down from the previous quarter’s share of 33.2%. Samsung once again grew its worldwide share, increasing from 17.2% last quarter to 22.3% this quarter. Samsung continues to work aggressively with carriers to drive tablet shipments through attractively priced smartphone bundles. Rounding out the top five were ASUS (5%), Lenovo (4.1%), and Amazon (1.9%).

“With roughly two-thirds share, Android continues to dominate the market,” said Jitesh Ubrani, Research Analyst, Worldwide Quarterly Tablet Tracker. “Although its share of the market remains small, Windows devices continue to gain traction thanks to sleeper hits like the Asus T100, whose low cost and 2-in-1 form factor appeal to those looking for something that’s ‘good enough’.”

Digitimes Research: Global tablet shipments reach 55.06 million units in 2Q14 [press release, July 23, 2014]

There were 55.06 million tablets shipped globally in the second quarter of 2014, decreasing 4.5% on quarter but increasing 17.9% on year, according to Digitimes Research.

The shipments consisted of 14.1 million iPads, down 10% on quarter, and 18.96 million units launched by vendors other than Apple, down 12.7% on quarter. Additionaly, 22.3 million white-box units were shipped in the second quarter.

Shipments of small-size Wi-Fi-enabled units in particular slowed down in the second quarter and the time period was also a slow season for shipments. Supply chains also faced yield issues and Samsung saw less-than-expected shipments for its 8-inch tablets. Tablets sized 10-inch and above have seen shipment increases since fourth-quarter 2014.

Taiwan tablet makers meanwhile surpassed 20 million in shipments for brand tablets during the second quarter, which made up 60% of overall brand tablet shipments during the time period, added Digitimes Research.

Digitimes Research: Global tablet shipments drop 30% sequentially in 1Q14 [press release, April 23, 2014]

Global tablet shipments reached only 58.56 million units in the first quarter of 2014, down almost 30% sequentially, but up 4.6% on year despite Samsung Electronics trying to boost both its high-end and entry-level tablet shipments and Lenovo pushing shipments to meet its fiscal 2013 targets. Seasonality, Apple seeing weaker sales, and the tablet market growing mature were also factors that affected shipment performance, according to Digitimes Research.

Shipments of iPads suffered both on-year and sequential drops to reach 15.85 million units in the first quarter. Non-iPad tablet shipments were 22.31 million units, down 20% sequentially, but up over 30% on year thanks to strong demand for Samsung, Lenovo and Asustek’s Windows-based models. White-box tablet shipments reached only 20.4 million units due to seasonality and labor shortages during the Lunar New Year holidays.

Apple and Samsung remained the top-two vendors in the first quarter, but the two players’ market share gap was less than 6pp. Lenovo was the third-largest vendor, followed closely by Asustek Computer in fourth. Amazon and Google dropped to number seven and ten.

Taiwan ODMs shipped 22.15 million tablets together in the first quarter, accounting for less than 60% of global shipments. The largest maker, Foxconn Electronics (Hon Hai Precision Industry), and second-largest Pegatron Technology both suffered significant shipment drops due to lower-than-expected demand for iPad. Quanta saw increased shipments in the quarter because of Asustek’s T100 tablet, and returned to being the third-largest maker in Taiwan. Compal Electronics’ shipments suffered a sharp decline because Amazon’s Kindle Fire range is approaching the end of its lifecycle, while Acer is turning to cooperate with China-based makers, Digitimes Research‘s figures showed.

Digitimes Research: Global white-box tablet shipments down in 1Q14 [press release, May 12, 2014]

There were 20.4 million white-box tablets shipped globally in the first quarter of 2014, decreasing by 27.4% on quarter and by 2.4% on year, according to Digitimes Research.

The decrease in shipments was mainly because most white-box vendors are based in China and there were fewer working days in the first quarter due to the Lunar New Year holidays, Digitimes Research pointed out.

Of the shipments, 7-inch models accounted for 70.5%, 7.85/7.9-inch ones 21.3%, 8- to 9-inch ones 4.2%, above 9- to 10-inch 2.9%, above 10-inch 1.1%.

Due to strong demand in emerging markets including India, Indonesia, Thailand, Russia and Eastern Europe, global white-box tablet shipments in the second quarter of 2014 will increase 14.2% on quarter and 45.6% on year to 23.3 million units.

2014 H1 changes on the Consumer Tablet Market in China

Versus as it was presented in Section I. of The lost U.S. grip on the mobile computing market, including not only the device business, but software development and patterns of use in general [this same blog, April 14, 2014]

Versus as it was presented in Section I. of The lost U.S. grip on the mobile computing market, including not only the device business, but software development and patterns of use in general [this same blog, April 14, 2014]

Justin Rosenstein of Asana: Be happy in a project-oriented teamwork environment made free of e-mail based communication hassle

Get Organized: Using Asana in Business [PCMag YouTube channel, Febr 24, 2014]

Steven Sinofsky, former head of Microsoft Office and (later) Windows at Microsoft:

We’ve all seen examples of the collaborative process playing out poorly by using email. There’s too much email and no ability to track and manage the overall work using the tool. Despite calls to ban the process, what is really needed is a new tool. So Asana is one of many companies working to build tools that are better suited to the work than one we currently all collectively seem to complain about.

in Don’t ban email—change how you work! [Learning by Shipping, Jan 31, 2014]

Asana is a simple example of an easy-to-use and modern tool that decreases (to zero) email flow, allows for everyone to contribute and align on what needs to be done, and to have a global view of what is left to do.

in You’re doing it wrong [Learning by Shipping, April 10, 2014] and Shipping is a Feature: Some Guiding Principles for People That Build Things [Learning by Shipping, April 17, 2014]

Making e-mail communication easier [Fox Business Video]

May. 06, 2014 – 3:22 – Asana co-founder Justin Rosenstein weighs in on his new email business.

How To Collaborate Effectively With Asana [Forbes YouTube channel, Feb 26, 2013]

Dustin Moskovitz: How Asana Gets Work Done [Forbes YouTube channel, Feb 26, 2013]

Do Great Things: Keynote by Justin Rosenstein of Asana | Disrupt NY 2014 [TechCrunch YouTube channel, May 5, 2014]

Asana’s Justin Rosenstein: “I Flew Coach Here.” | Disrupt NY 2014 [TechCrunch YouTube channel, May 5, 2014]

How we use Asana [asana blog, Oct 9, 2013]

We love to push the boundaries of what Asana can do. From creating meeting agendas to tracking bugs to maintaining snacks in the refrigerator, the Asana product is (unsurprisingly) integral to everything we do at Asana. We find many customers are also pushing the boundaries of Asana to fit their teams’ needs and processes. Since Asana was created to be flexible and powerful enough for every team, nothing makes us more excited than hearing about these unique use cases.

Recently, we invited some of our Bay Area-based customers to our San Francisco HQ to share best practices with one another and hear from our cofounder Justin Rosenstein about the ways we use Asana at Asana. We’re excited to pass on this knowledge through some video highlights from the event. You can watch the entire video here: The Asana Way to Coordinate Ambitious Projects with Less Effort

Capture steps in a Project

“The first thing we always do is create a Project that names what we’re trying to accomplish. Then we’ll get together as a team and think of, ‘What is every single thing we need to accomplish between now and the completion of that Project?’ Over the course of the Project, all of the Tasks end up getting assigned.”Organize yourself

“Typically when I start my day, I’ll start by looking at all the things that are assigned to me. I’ll choose a few that I want to work on today. I try to be as realistic as possible, which means adding half as many things as I am tempted to add. After putting those into my ‘Today’ view, there are often a couple of other things I need to do. I just hit enter and add a few more tasks.”Forward emails to Asana

“Because I want Asana to be the source of truth for everything I do, I want to put emails into my task list and prioritize them. I’ll just take the email and forward it to x@mail.asana.com. We chose ‘x’ so it wouldn’t conflict with anything else in your address book. Once I send that, it will show up in Asana with the attachments and everything right intact.”Run great meetings

“We maintain one Project per meeting. If I’m looking at my Task list and see a Task I want to discuss at the meeting, I’ll just use Quick Add (tab + Q) to put the Task into the correct Project. Then when the meeting comes around, everything that everyone wants to talk about has already been constructed ahead of time.”Track responsibility

“Often a problem comes up and someone asks, ‘Who’s responsible for that?’ So instead, we’ve built out a list of areas of responsibility (AoRs), which is all the things that someone at the company has to be responsible for. By having AoRs, we distribute responsibility. We can allow managers to focus on things that are more specific to management and empower everyone at the company to be a leader in their own field.”

Background on https://asana.com/

|

Asana |

About Us |

|

Connect |

Support |

How it all started and progressed?

asana demo & vision talk [Robert Marquardt YouTube channel, Feb 15, 2011]

The Asana Vision & Demo [asana blog, Feb 7, 2011]

We recently hosted an open house at our offices in San Francisco, where we showed the first public demo of Asana and deep-dived into the nuances of the product, the long-term mission that drives us, how the beta’s going, and more. We were really excited to be able to share what we’ve been working on and why we’re so passionate about it, and hope you enjoy

thisthe above video of the talk:Asana will be available more broadly later this year. In the meantime,

- if you’re interested in participating in the beta program, sign up here.

- if these sound like problems you’d like to help tackle, we’re hiring.

- and if you’d just like to receive updates about Asana going forward, use the form in the upper right of this page.

Introducing Asana: The Modern Way to Work Together [asana blog, Nov 2, 2011]

…

Asana is a modern web application that keeps teams in sync, a shared task list where everyone can capture, organize, track, and communicate what they are working on in service of their common goal. Rather than trying to stay organized through the tedious grind of emails and meetings, teams using Asana can move faster and do more — or even take on bigger and more interesting goals.

…How Asana Works:

Asana re-imagines the way we work together by putting the fundamental unit of productivity – the task – at the center. Breaking down ambitious goals into small pieces, assigning ownership of those tasks, and tracking them to completion is how things get built, from software to skyscrapers. With Asana, you can:

- capture everything your team is planning and doing in one place. When tasks and the conversations about them are collected together, instead of spread around emails, documents, whiteboards, and notebooks, they become the shared, trusted, collective memory for your organization.

- keep your team in sync on the priorities, and what everyone is working on. When you have a single shared view of a project’s priorities, along with an accurate view into what each person is working on and when, everyone on the team knows exactly what matters, and what work remains between here and the goal.

- get the right information at the right time. Follow tasks, and you’ll receive emails as their status evolves. Search, and you’ll see the full activity feed of all the discussions and changes to a task over its history. Now, it’s easy to stay on top of the details — without asking people to forward you a bunch of email threads.

…

Building tools for teamwork [asana blog, Nov 22, 2013]

Our co-founder, Justin, recently wrote in Wired about why we need to rethink the tools we use to work together. The article generated a lot of interesting comments, from ideas on knowledge management to fatigue with the “meeting lifestyle,” to this protest on the typical office culture:

“Isn’t the root of this problem that, within our own organizations, we fiercely guard information and our decision-making processes? Email exchanges and invite-only meetings shut out others– forcing the need for follow-up conversations, summary reports, and a trail of other status/staff meetings to relay content already covered some place/some time before.”

To reach its goals, we think a team needs clarity of purpose, plan and responsibility. Technology and tools can help us reach that kind of clarity, but only if they target the right problem. From their roles at Facebook, Asana’s founders have extensive knowledge of social networks, and the social graph technology they rely on. But Asana isn’t a social network. Why? Because, as Justin outlines, the social graph doesn’t target the problem of work:

Our personal and professional lives, even if they overlap, have two distinct goals — and they require different “graphs.”

For our personal lives, the goal is love (authentic interpersonal connection), and that requires a social graph with people at the center. For our work lives, the goal is creation (working together to realize our collective potential), and that requires a work graph, with the work at the center.

Don’t get me wrong: Human connection is valuable within a business. But it should be in service to the organizational function of getting work done, and doesn’t need to be the center of the graph.

So, how does this change the experience for you and your teammates? A work graph means having all the information you need when you need it. Instead of blasting messages at the whole team, like “Hey, has anyone started working on this yet?”, you should be able to efficiently find out exactly who’s working on that task and how much progress they’ve made. That’s the target Asana is aiming for. Read Justin’s full Wired article.

Organizations in Asana [asana blog, May 1, 2013]

Today, we’re excited to be launching a collection of new features aimed at helping companies use and support Asana across their entire enterprise. We call it Organizations.

Since we began, Asana has been on a mission to help great teams achieve more ambitious goals. We started 18 months ago with our free service, targeted at smaller teams and even individuals – helping them get and stay organized.

When we launched our first premium tiers six months later, we enabled medium sized teams and companies – think 10s to 100s of people – to go further with Asana. In the year between then and now, we’ve been continuously amazed by all the places and ways Asana is being used to organize a team: in industries as diverse as education, healthcare, finance, technology, and manufacturing; in companies from two-person partnerships to Fortune 100 enterprises; and in dozens of countries representing every continent but the frozen one. There’s a lot of important work being organized in Asana.

But we’re still just getting started – there remain teams that we haven’t been ready to support: the largest teams, those that grow from 100s to 1,000s of people. While it would be remarkable if it only took a small number of coworkers to design and manufacture electric cars, synthesize DNA, or deliver healthcare to villages across the globe – these missions are complex, and require more people to be involved in them to succeed. Many of the teams using Asana today are inside these bigger organizations, and they’ve been asking for Asana to work at enterprise-scale. So for the past several months, we’ve been working on just that.

…

Stories from our first year [asana blog, Nov 12, 2012]

… When we launched a year go, we had an ambitious mission: to create a shared task management platform that empowers teams of like-minded people to do great things. … In the course of our first year, tens of thousands of teams looking for a better way to work together have adopted Asana. …

… we collected three of these stories from three distinct kinds of teams:

– a tech startup [Foursquare],

– a fast-growing organic food company [Bare Fruit & Sundia] and

– a leading Pacific Coast aquarium [Aquarium of the Bay].…

Foursquare Launches 5.0

Right around the time Foursquare passed 100 employees over the last year, we started building Foursquare 5.0. This update was a big deal: we were overhauling Foursquare’s core mechanics, evolving from check-ins towards the spontaneous discovery of local businesses. As we built the new app, we needed a way to gather feedback from the entire team.

We tried what felt like every collaboration tool around. Group emails were a mess. Google Docs was impossible to parse. We’d heard about Asana and decided to give it a shot.

Using Asana, we were easily able to collect product feedback and bugs from everyone in the company, then parse, discuss, distribute and prioritize the work. It became an indispensable group communication tool.

Foursquare 5.0 was a giant success, and we couldn’t have done it without Asana.

–Noah Weiss, Product Manager

…

Then, Of Course, There Is Us

It’s an understatement to say that we rely on Asana. We use our own product to manage every function of our business. Asana is where we plan, capture ideas, build meeting agendas, prioritize our product roadmap, document which bugs to fix and list the snacks to buy. It’s our CRM, our editorial calendar, our Applicant Tracking System, and our new-hire orientation system. Every team in the company – from product, design, and engineering to sales and marketing to recruiting and user operations – relies on the product we are building to stay in sync, connect our individual tasks to the bigger picture and accomplish our collective goals.

…

Q&A: Rising Realty Partners builds their business with Asana [asana blog, Feb 7, 2014]

…The Los Angeles development firm Rising Realty Partners, shared with us how they used Asana, and our integration with Dropbox, to close a massive ten-property deal.

As our business expanded, we found ourselves relying heavily on email, faxes, and even FedEx to communicate with each other and collaborate with outside parties. We needed a better way to organize, prioritize and communicate around our work, and we found the answer in Asana.

…

I can’t image how complex our communications would have been if we weren’t using Asana. We had dozens of people internally, and more than 50 people externally, all involved in making this deal happen. Having all of that communication in Asana significantly cut down on the craziness.

…

Because of Asana’s Dropbox integration, our workflow is now fast, intuitive and organized — something that was impossible to achieve over email. For the acquisition, we used Asana and Dropbox simultaneously to keep track of everything; from what each team member was doing, to the current status of each transaction, to keeping a history of all related documents. We had more than 18,000 items in Dropbox that we would link to in Asana instead of attaching them in email. We removed more than 30 gigabytes of information per recipient from our inboxes and everything was neatly organized around the work we were doing in Asana. This meant that the whole team always had the latest and most relevant information.

…For this entire project, maybe one percent of our total internal communication was happening in email. With Asana, anyone in the company could look at any aspect of the project, see where it stood, and add their input. No one had to remember to cc’ or ‘reply all’.

….

The success of this deal was largely due to Asana and we plan to use it in future acquisitions –Asana has become essential to our team’s success.

….

Our iPhone App Levels Up [asana blog, Sept 6, 2012]

Until recently, we’ve focused most of our energy on the browser-based version of Asana. But, in the last few months, even as we’ve launched major new features in our web application, we’ve been putting much more time into improving the mobile experience. In June, we made several meaningful architectural improvements to pave the way for bigger and better things and hinted that these changes were in the works.

Today, we’ve taken the next step in that direction: Version 2.0 of our iPhone app is in the App Store now. We are really proud of this effort – almost everyone at Asana played a part in this release. This new version is a top-to-bottom redesign that really puts the power of the desktop web version of Asana right in your pocket.

…

Asana comes to Android [asana blog, Feb 28, 2013]

Five months ago, we launched our first bonafide mobile app, for the iPhone, and we’ve been steadily improving it ever since. Focusing on a single platform at first allowed us to be meticulous about our mobile experience, adding new features and honing the design until we knew it was something people loved. After strong positive feedback from our customers and a solid rating in the iTunes App Store, we knew it was time.

Today, we are happy to announce that Asana for Android is here. You can get it right now in the Google Play store

…

As of today (May 8, 2014) there are 70 employees and 15 open positions. The company has 4 investors: Benchmark Capital, Andreessen-Horowitz, Founders Fund and Peter Thiel. The first two put $9 million in November 2009. Then Founders Fund and Peter Thiel added to that $28 million in July 2012. Reuters reported that with Facebook alumni line up $28 million for workplace app Asana [July 23, 2012]:

Asana, a Silicon Valley start-up, has lined up $28 million in a financing round led by PayPal co-founder Peter Thiel and his Founders Fund, the company said.

The funding round values the workplace-collaboration company at $280 million, a person familiar with the matter said.

“This investment allows us to attract the best and brightest designers and engineers,” said Asana co-founder Justin Rosenstein, who said that in turn would help the company build on its goal of making interaction among its client-companies’ employees easier.

Asana launched the free version last year of its company management software that makes it easier to collaborate on projects. It introduced a paid, premium service earlier this year. It declined to give revenue figures, but said “hundreds” of customers had upgraded to the premium version.

Although Rosenstein and co-founder Dustin Moskovitz are alumni of social-network Facebook– Moskovitz co-founded the service with his Harvard roommate Mark Zuckerberg – they were quick to distance Asana from social networking.

Instead, they say, they view the company as an alternative to email, in-person meetings, physical whiteboards, and spreadsheets.

“That’s what we see as our competition,” said Rosenstein. “Replacing those technologies.”

With its latest funding round, Asana has now raised a total of $38 million from investors including Benchmark Capital and Andreessen Horowitz.

Thiel, who got to know Moskovitz and Rosenstein thanks to his early backing of Facebook, had already invested in Asana when it raised its “angel” round in early 2009. Now, his high-profile Founders Fund is investing and Thiel is joining Asana’s board.

Facebook has 901 million monthly users and revenue last year of $3.7 billion. But its May initial public offering disappointed many investors after it priced at $38 per share and then quickly fell. It closed on Friday at $28.76.

Many investors speculate that start-ups will have to accept lower valuations in the wake of the Facebook IPO. The Asana co-founders said the terms of their latest funding round were set before Facebook debuted on public markets.

A few of Facebook’s longtime employees have gone on to work on their own ventures.

Bret Taylor, formerly chief technology officer, said last month he was leaving to start his own company.

Dave Morin, who joined Facebook in 2008 from Apple, left in 2010 to found social network Path. Facebook alumni Adam D’Angelo and Charlie Cheever left in 2009 to start Quora, their question-and-answer company, which is also backed by Thiel.

Another former roommate of Zuckerberg’s, Chris Hughes, also left a few years ago and coordinated online organizing for Barack Obama’s 2008 presidential campaign. Now, he is publisher of the New Republic magazine.

Matt Cohler, who joined Facebook from LinkedIn early in 2005, joined venture capital firm Benchmark Capital in 2008. His investments there include Asana and Quora.

Core technology used

Luna, our in-house framework for writing great web apps really quickly [asana blog, Feb 2, 2010]

At Asana, we’re building a Collaborative Information Manager that we believe will make it radically easier for groups of people to get work done. Writing a complex web application, we experienced pain all too familiar to authors of “Web 2.0″ software (and interactive software in general): there were all kinds of extremely difficult programming tasks that we were doing over and over again for every feature we wanted to write. So we’re developing Lunascript — an in-house programming language for writing rich web applications in about 10% of the time and code you can today.

Check out the

videowe made »

[rather an article about Luna as of Nov 2, 2011]

Update: For now we’ve tabled using the custom DSL syntax in favor of a set of Javascript idioms and conventions on top of the “Luna” runtime. So while the contents of this post still accurately present the motivation and capabilities of the Luna framework, we’re using a slightly more cumbersome (JavaScript) syntax than what you see below, in exchange for having more control over the “object code” (primarily for hand-tuning performance).

Release the Kraken! An open-source pub/sub server for the real-time web [asana blog, March 5, 2013]

Today, we are releasing Kraken, the distributed pub/sub server we wrote to handle the performance and scalability demands of real-time web apps like Asana.

…

Before building Kraken, we searched for an existing open-source pub/sub solution that would satisfy our needs. At the time, we discovered that most solutions in this space were designed to solve a much wider set of problems than we had, and yet none were particularly well-suited to solve the specific requirements of real-time apps like Asana. Our team had experience writing routing-based infrastructure and ultimately decided to build a custom service that did exactly what we needed – and nothing more.The decision to build Kraken paid off. For the last three years, Kraken has been fearlessly routing messages between our servers to keep your team in sync. During this time, it has yet to crash even once. We’re excited to finally release Kraken to the community!

Issues Moving to Amazon’s Elastic Load Balancer [asana blog, June 5, 2012]

…

Asana’s infrastructure runs almost entirely on top of Amazon Web Services (AWS). AWS provides us with the ability to launch managed production infrastructure in minutes with simple API calls. We use AWS for servers, databases, monitoring, and more. In general, we’ve been very happy with AWS. A month ago, we decided to use Amazon’s Elastic Load Balancer service to balance traffic between our own software load balancers.

…

Announcing the Asana API [asana blog, April 19, 2012]

Today we are excited to share that you can now add and access Asana data programmatically using our simple REST API.

The Asana API lets you build a variety of applications and scripts to integrate Asana with your business systems, show Asana data in other contexts, and create tasks from various locations.

Here are some examples of the things you can build:

- Source Control Integration to mark a Task as complete and add a link to the code submission as a comment when submitting code.

- A desktop app that shows the Tasks assigned to you

- A dashboard page that shows a visual representation of complete and incomplete Tasks in a project

…

Asana comes to Internet Explorer [asana blog, Oct 16, 2013]

…

Asana is a fast and versatile web-based application that pushes the boundaries of what’s possible inside a browser. Our sophisticated Javascript app requires a modern browser platform, and up until now we could only provide the right user experience on Chrome, Firefox, and Safari. With IE10, Internet Explorer has drastically improved their developer tools and made a marked improvement in standards compliance. With these improvements, we were able to confidently develop Asana for IE10, and we’ve been pleasantly surprised by the process. Check out the blog post on our developer site to see what we learned during this project.

…

Microsoft BUILD 2014 Day 2: “rebranding” to Microsoft Azure and moving toward a comprehensive set of fully-integrated backend services

- “Rebranding” into Microsoft Azure from the previous Windows Azure

- Microsoft Azure Momentum on the Market

- The new Azure Management Portal (preview)

- New Azure features: IaaS, web, mobile and data announcements

Microsoft Announces New Features for Cloud Computing Service [CCTV America YouTube channel, April 3, 2014]

Day two of the Microsoft Build developer conference in San Francisco wrapped up with the company announcing 44 new services. Most of those are based on Microsoft Azure – it’s cloud computing platform that manages applications across data centers. CCTV’s Mark Niu reports from San Francisco.

Watch the first 10 minutes of this presentation for a brief summary of the latest state of Microsoft Azure: #ChefConf 2014: Mark Russinovich, “Microsoft Azure Group” [Chef YouTube channel, April 16, 2014]

Then here is a fast talk and Q&A on Azure with Scott Guthrie after his keynote preseantation at BUILD 2014:

Cloud Cover Live – Ask the Gu! [jlongo62 YouTube channel, published on April 21, 2014]

The original: Cloud Cover Live – Ask the Gu! [Channel 9, April 3, 2014]

Details:

- “Rebranding” into Microsoft Azure from the previous Windows Azure

- Microsoft Azure Momentum on the Market

- The new Azure Management Portal (preview)

- New Azure features: IaaS, web, mobile and data announcements

[2:45:47] long video record of the Microsoft Build Conference 2014 Day 2 Keynote [MSFT Technology News YouTube channel, recorded on April 3, published on April 7, 2014]

The original video record on Channel 9

Day 2 Keynote transcript by Microsoft

1. “Rebranding” into Microsoft Azure from the previous Windows Azure

Yes, you’ve noticed right: the Windows prefix has gone, and the full name is now only Microsoft Azure! The change happened on April 3 as evidenced by change of the cover photo on the Facebook site, now also called Microsoft Azure:

from this cover photo used from July 23, 2013 on:

And it happened without any announcement or explanation as even the last, April 1 Microsoft video carried the Windows prefix: Tuesdays with Corey //build Edition

as well as the last, March 14 video ad: Get Your Big Bad Wolf On (Extended)

2. Microsoft Azure Momentum on the Market

The day began with Scott Guthrie, Executive Vice President, Microsoft Cloud and Enterprise group, touting Microsoft progress with Azure for the last 18 months when:

… we talked about our new strategy with Azure and our new approach, a strategy that enables me to use both infrastructure as a service and platform as a service capabilities together, a strategy that enables developers to use the best of the Windows ecosystem and the best of the Linux ecosystem together, and one that delivers unparalleled developer productivity and enables you to build great applications and services that work with every device …

- Last year … shipped more than 300 significant new features and releases

- … we’ve also been hard at work expanding the footprint of Azure around the world. The green circles you see on the slide here represent Azure regions, which are clusters of datacenters close together, and where you can go ahead and run your application code. Just last week, we opened two new regions, one in Shanghai and one in Beijing. Today, we’re the only global, major cloud provider that operates in mainland China. And by the end of the year, we’ll have more than 16 public regions available around the world, enabling you to run your applications closer to your customers than ever before.

- More than 57 percent of the Fortune 500 companies are now deployed on Azure.

- Customers run more than 250,000 public-facing websites on Azure, and we now host more than 1 million SQL databases on Azure.

- More than 20 trillion objects are now stored in the Azure storage system. We have more than 300 million users, many of them — most of them, actually, enterprise users, registered with Azure Active Directory, and we process now more than 13 billion authentications per week.

- We have now more than 1 million developers registered with our Visual Studio Online service, which is a new service we launched just last November.

Let’s go beyond the big numbers, though, and look at some of the great experiences that have recently launched and are using the full power of Azure and the cloud.

“Titanfall” was one of the most eagerly anticipated games of the year, and had a very successful launch a few weeks ago. “Titanfall” delivers an unparalleled multiplayer gaming experience, powered using Azure.

Let’s see a video of it in action, and hear what the developers who built it have to say.

[Titanfall and the Power of the Cloud [xbox YouTube channel, April 3, 2014]]

One of the key bets the developers of “Titanfall” made was for all game sessions on the cloud. In fact, you can’t play the game without the cloud, and that bet really paid off.

As you heard in the video, it enables much, much richer gaming experiences. Much richer AI experiences. And the ability to tune and adapt the game as more users use it.

To give you a taste of the scale, “Titanfall” had more than 100,000 virtual machines deployed and running on Azure on launch day. Which is sort of an unparalleled size in terms of a game launch experience, and the reviews of the game have been absolutely phenomenal.

Another amazing experience that recently launched and was powered using Azure was the Sochi Olympics delivered by NBC Sports.

NBC used Azure to stream all of the games both live and on demand to both Web and mobile devices. This was the first large-scale live event that was delivered entirely in the cloud with all of the streaming and encoding happening using Azure.

Traditionally, with live encoding, you typically run in an on-premises environment because it’s so latency dependent. With the Sochi Olympics, Azure enabled NBC to not only live encode in the cloud, but also do it across multiple Azure regions to deliver high-availability redundancy.

More than 100 million people watched the online experience, and more than 2.1 million viewers alone watched it concurrently during the U.S. versus Canada men’s hockey match, a new world record for online HD streaming.

…

RICK CORDELLA [Senior Vice President and General Manager of NBC Sports Digital]: The company bets about $1 billion on the Olympics each time it goes off. And we have 17 days to recoup that investment. Needless to say, there is no safety net when it comes to putting this content out there for America to enjoy. We need to make sure that content is out there, that it’s quality, that our advertisers and advertisements are being delivered to it. There really is no going back if something goes wrong.

…

The decision for that was taken more than a year ago: Windows Azure Teams Up With NBC Sports Group [Microsoft Azure YouTube channel, April 9, 2013]

3. The new Azure Management Portal (preview)

But in fact a new way of providing a comprehensive set of fully-integrated backend services had significantly bigger impact on the audience of developers. According to Microsoft announces new cloud experience and tools to deliver the cloud without complexity [The Official Microsoft Blog, April 3, 2014]

The following post is from Scott Guthrie, Executive Vice President, Cloud and Enterprise Group, Microsoft.

On Thursday at Build in San Francisco, we took an important step by unveiling a first-of-its kind cloud environment within Microsoft Azure that provides a fully integrated cloud experience – bringing together cross-platform technologies, services and tools that enable developers and businesses to innovate with enterprise-grade scalability at startup speed. Announced today, our new Microsoft Azure Preview [Management]Portal is an important step forward in delivering our promise of the cloud without complexity.

When cloud computing was born, it was hailed as the solution that developers and business had been waiting for – the promise of a quick and easy way to get more from your business-critical apps without the hassle and cost of infrastructure. But as the industry transitions toward mobile-first, cloud-first business models and scenarios, the promise of “quick and easy” is now at stake. There’s no question that developing for a world that is both mobile-first and cloud-first is complicated. Developers are managing thousands of virtual machines, cobbling together management and automation solutions, and working in unfamiliar environments just to make their apps work in the cloud – driving down productivity as a result.

Many cloud vendors tout the ease and cost savings of the cloud, but they leave customers without the tools or capabilities to navigate the complex realities of cloud computing. That’s why today we are continuing down a path of rapid innovation. In addition to our groundbreaking new Microsoft Azure Preview [Management] Portal, we announced several enhancements our customers need to fully tap into the power of the cloud. These include:

- Dozens of enhancements to our Azure services across Web, mobile, data and our infrastructure services

- Further commitment to building the most open and flexible cloud with Azure support for automation software from Puppet Labs and Chef.

- We’ve removed the throttle off our Application Insights preview, making it easier for all developers to build, manage and iterate on their apps in the cloud with seamless integration into the IDE

<For details see the separate section 4. New Azure features: IaaS, web, mobile and data announcements>

Here is a brief presentation by a Brazilian specialist: Microsoft Azure [Management] Portal First Touch [Bruno Vieira YouTube channel, April 3, 2014]

From Microsoft evolves the cloud experience for customers [press release, April 3, 2014]

… Thursday at Build 2014, Microsoft Corp. announced a first-of-its-kind cloud experience that brings together cross-platform technologies, services and tools, enabling developers and businesses to innovate at startup speed via a new Microsoft Azure Preview [Management] Portal.

In addition, the company announced several new milestones in Visual Studio Online and .NET that give developers access to the most complete platform and tools for building in the cloud. Thursday’s announcements are part of Microsoft’s broader vision to erase the boundaries of cloud development and operational management for customers.

“Developing for a mobile-first, cloud-first world is complicated, and Microsoft is working to simplify this world without sacrificing speed, choice, cost or quality,” said Scott Guthrie, executive vice president at Microsoft. “Imagine a world where infrastructure and platform services blend together in one seamless experience, so developers and IT professionals no longer have to work in disparate environments in the cloud. Microsoft has been rapidly innovating to solve this problem, and we have taken a big step toward that vision today.”

One simplified cloud experience

The new Microsoft Azure Preview [Management] Portal provides a fully integrated experience that will enable customers to develop and manage an application in one place, using the platform and tools of their choice. The new portal combines all the components of a cloud application into a single development and management experience. New components include the following:

Simplified Resource Management. Rather than managing standalone resources such as Microsoft Azure Web Sites, Visual Studio Projects or databases, customers can now create, manage and analyze their entire application as a single resource group in a unified, customized experience, greatly reducing complexity while enabling scale. Today, the new Azure Manager is also being released through the latest Azure SDK for customers to automate their deployment and management from any client or device.

Integrated billing. A new integrated billing experience enables developers and IT pros to take control of their costs and optimize their resources for maximum business advantage.

Gallery. A rich gallery of application and services from Microsoft and the open source community, this integrated marketplace of free and paid services enables customers to leverage the ecosystem to be more agile and productive.

Visual Studio Online. Microsoft announced key enhancements through the Microsoft Azure Preview [Management] Portal, available Thursday. This includes Team Projects supporting greater agility for application lifecycle management and the lightweight editor code-named “Monaco” for modifying and committing Web project code changes without leaving Azure. Also included is Application Insights, an analytics solution that collects telemetry data such as availability, performance and usage information to track an application’s health. Visual Studio integration enables developers to surface this data from new applications with a single click.

…

Building an open cloud ecosystem

Showcasing Microsoft’s commitment to choice and flexibility, the company announced new open source partnerships with Chef and Puppet Labs to run configuration management technologies in Azure Virtual Machines. Using these community-driven technologies, customers will now be able to more easily deploy and configure in the cloud. In addition, today Microsoft announced the release of Java Applications to Microsoft Azure Web Sites, giving Microsoft even broader support for Web applications.

…

From BUILD Day 2: Keynote Summary [by Steve Fox – DPE (MSFT) on MSDN Blogs, April 3, 2014]

….

Bill Staples then came on stage to show off the new Azure [management] portal design and features. Bill walked through a number of the new innovations in the portal, such as improved UX, app insights, “blade” views [the “blade” term is used for the dropdown that allows a drilldown], etc. A screen shot of the new portal is shown below.

Bill also walked through the comprehensive analytics (such as compute and billing) that are now available on the portal. He also walked through “Application Insights,” which is a great way to instrument your code in both the portal and in your code with easy-to-use, pre-defined code snippets. He completed his demo walkthrough by showing the Azure [management] portal as a “NOC” [Network Operations Center] view on a big-screen TV.

…

The above image is at the [1:44:24] point in time of the keynote video record on Channel 9 and it is giving more information if we provide here the part of transcript around it:

BILL STAPLES at [1:43:39]: Now, to conclude the operations part of this demo, I wanted to show you an experience for how the new Azure Portal works on a different device. You’ve seen it on the desktop, but it works equally well on a tablet device, that is really touch friendly. Check it out on your Surface or your iPad, it works great on both devices.

But we’re thinking as well if you’ve got a big-screen TV or a projector lying around your team room, you might want to think about putting the Microsoft Azure portal as your own personal NOC.

In this case, I’ve asked the Office developer team if we could have access to their live site log. So they made me promise, do not hit the stop button or the delete button, which I promised to do.

[1:44:24] This is actually the Office developer log site. And you can see it’s got almost 10 million hits already today running on Azure Websites. So very high traffic.

They’ve customized it to show off the browser usage on their website. Imagine we’re in a team Scrum with the Office developer guys and we check out, you know, how is the website doing? We’ve got some interesting trends here.

In fact, there was a spike of sessions it looks like going on about a week ago. And page views, that’s kind of a small part. It would be nice to know which page it was that spiked a week ago. Let’s go ahead and customize that.

This screen is kind of special because it has touch screen. So I can go ahead and let’s make that automatically expand there. Now we see a bigger view. Wow, that was a really big spike last week. What page was that? We can click into it. We get the full navigation experience, same on the desktop, as well as, oh, look at that. There’s a really popular blog post that happened about a week ago. What was that? Something about announcing Office on the iPad you love. Makes sense, huh? So we can see the Azure Portal in action here as the Office developer team might imagine it. [1:45:44]

The last thing I want to show is the Azure Gallery.

We populated the gallery with all of the first-party Microsoft Azure services, as well as the [services from] great partners that we’ve worked with so far in creating this gallery.

And what you’re seeing right here is just the beginning. We’ve got the core set of DevOps experiences built out, as well as websites, SQL, and MySQL support. But over the coming months, we’ll be integrating all of the developer and IT services in Microsoft as well as the partner services into this experience.

Let me just conclude by reminding us what we’ve seen. We’ve seen a first-of-its-kind experience from Microsoft that fuses our world-class developer services together with Azure to provide an amazing dev-ops experience where you can enjoy the entire lifecycle from development, deployment, operations, gathering analytics, and iterating right here in one experience.

We’ve seen an application-centric experience that brings together all the dev platform and infrastructure services you know and love into one common shell. And we’ve seen a new application model that you can describe declaratively. And through the command line or programmatically, build out services in the cloud with tremendous ease. [1:47:12]

More information on the new Azure [Management] Portal:

- From Visual Studio Online Integration in the Azure [management] portal [by Brian Harry (MSFT) on MSDN Blogs, April 3, 2014]

Today, at Build, we unveiled a new Azure [Management] Portal experience we are building. I want to give you some insights into the work that VS Online team is doing to help with it. I’m not on the Azure team and am no expert on how they’d like to describe to the world, so please take any comments I make here about the new Azure portal as my perspective on it and not necessarily an official one.

Bill Staples first presented to me almost a year ago an idea of creating a new portal experience for Azure designed to be an optimal experience for DevOps. It would provide everything a DevOps team needs to do modern cloud based development. Capabilities to provision dev and test resources, development and collaboration capabilities, build, release and deployment capabilities, application telemetry and management capabilities and more. Pretty quickly it became clear to me that if we could do it, it would be awesome. An incredibly productive and easy way for devs to do soup to nuts app development.

What we demoed today (and made available via http://portal.azure.com”) is the first incarnation of that. My team (the VS Online Team) has worked very hard over the past many months with the Azure team to build the beginnings of the experience we hope to bring to you. It’s very early and it’s nowhere near done but it’s definitely something we’d love to start getting some feedback on.

For now, it’s limited to Azure websites, SQL databases and a subset of the VS Online capabilities. If you are a VS Online/TFS user, think of this as a companion to Visual Studio, Visual Studio Online and all of the tools you are used to. When you create a team project in the Azure portal, it’s a VS Online Team Project like any other and is accessible from the Azure portal, the VS Online web UI, Visual Studio, Eclipse and all the other ways your Visual Studio Online assets are available. For now, though, there are a few limitations – which we are working hard to address. We are in the middle of adding Azure Active Directory support to Visual Studio Online and, for a variety of reasons, chose to limit the new portal to only work with VS Online accounts linked to Azure Active Directory.

The best way to ensure this is just to create a new Team Project and a new VS Online account from within the new Azure portal. You will need to be logged in to the Azure portal with an identity known to your Azure Active Directory tenant and to add new users, rather than add them directly in Visual Studio Online, you will add them through Azure Active directory. One of the ramifications of this, for now, is that you can’t use an existing VS Online account in the new portal – you must create a new one. Clearly that’s a big limitation and one we are working hard to remove. We will enable you to link existing VS Online accounts to Active Directory we just don’t have it yet – stay tuned.

I’ll do a very simple tour. You can also watch Brian Keller’s Channel9 video.

…

- Enabling DevOps with Azure and Visual Studio Online [jlongo62 YouTube channel, published on April 21, 2014]

Further information:

- Building your Dream DevOps Dashboard with the new Azure Preview Portal [by Brian Keller [MSFT] on MSDN Blogs, April 10, 2014]

- Azure [Management] Portal Preview and Visual Studio Online: Adding a user [by Buck Hodges (MSFT) on MSDN Blogs, April 3, 2014]

4. New Azure features: IaaS, web, mobile and data announcements

According to Scott Guthrie, Executive Vice President, Microsoft Cloud and Enterprise group:

[IaaS] First up, let’s look at some of the improvements we’re making with our infrastructure features and some of the great things we’re enabling with virtual machines.

Azure enables you to run both Windows and Linux virtual machines in the cloud. You can run them as stand-alone servers, or join them together to a virtual network, including one that you can optionally bridge to an on-premises networking environment.

This week, we’re making it even easier for developers to create and manage virtual machines in Visual Studio without having to leave the VS IDE: You can now create, destroy, manage and debug any number of VMs in the cloud. (Applause.)

Prior to today, it was possible to create reusable VM image templates, but you had to write scripts and manually attach things like storage drives to them. Today, we’re releasing support that makes it super-easy to capture images that can contain any number of storage drives. Once you have this image, you can then very easily take it and create any number of VM instances from it, really fast, and really easy. (Applause.)

Starting today, you can also now easily configure VM images using popular frameworks like Puppet, Chef, and our own PowerShell and VSD tools. These tools enable you to avoid having to create and manage lots of separate VM images. Instead, you can define common settings and functionality using modules that can cut across every type of VM you use.

You can also create modules that define role-specific behavior, and all these modules can be checked into source control and they can also then be deployed to a Puppet Master or Chef server.

And one of the things we’re doing this week is making it incredibly easy within Azure to basically spin up a server farm and be able to automatically deploy, provision and manage all of these machines using these popular tools.

…

We’re also excited to announce the general availability of our auto-scale service, as well as a bunch of great virtual networking capabilities including point-to-site VPN support going GA, new dynamic routing, subnet migration, as well as static internal IP address. And we think the combination of this really gives you a very flexible environment, as you saw, a very open environment, and lets you run pretty much any Windows or Linux workload in the cloud.

So we think infrastructure as a service is super-flexible, and it really kind of enables you to manage your environments however you want.

We also, though, provide prebuilt services and runtime environments that you can use to assemble your applications as well, and we call these platform as a service [PaaS] capabilities.

One of the benefits of these prebuilt services is that they enable you to focus on your application and not have to worry about the infrastructure underneath it.

We handle patching, load balancing, high availability and auto scale for you. And this enables you to work faster and do more.

What I want to do is just spend a little bit of time talking through some of these platform as a service capabilities, so we’re going to start talking about our Web functionality here today.

[Web] One of the most popular PaaS services that we now have on Windows Azure is something we call the Azure Website Service. This enables you to very easily deploy Web applications written in a variety of different languages and host them in the cloud. We support .NET, NOJS, PHP, Python, and we’re excited this week to also announce that we’re adding Java language support as well.

This enables you as a developer to basically push any type of application into Azure into our runtime environment, and basically host it to any number of users in the cloud.

Couple of the great features we have with Azure include auto-scale capability. What this means is you can start off running your application, for example, in a single VM. As more load increases to it, we can then automatically scale up multiple VMs for you without you having to write any script or take any action yourself. And if you get a lot of load, we can scale up even more.